Heart mine which is that of my Mother, Whole Heart mine which is that of my birth, Let there be no estoppel[1]against me through evidence, let no hindrance be made to me by the divine Circle; fall thou not against me in presence of him who is at the Balance . Thou art my Genius, who art by me, the Artistwho givest soundness to my limbs. Come forth to the bliss towards which we are bound; Let not those Ministrantswho deal with a man according to the course of his lifegive a bad odour to my name.[2]Pleasant for us, pleasant for the listener, is the joy of the Weighing 𓍝 of the Words. Let not lies be uttered in presence of the great god. Lord of the Amenta.* Lo! how great art thou as the Triumphant one.

* amenta: the Duat or Underworld, hieroglyph 𓇽 ; in Neapolitan (Kingdom of Naples) dialect: “mint” (coins). Plural of āmentum: a sandal-strap (Egyptian 𓋹 “Life”), band or thong, especially on a missile weapon.

Compare the Pentalpha “star” (Egyptian 𓇼 dawn sun) engraved stone ring in the Testament of Solomon, for command over “male and female” demons.[4]

An alternate form of capital Omega Ω resembles an underlined superscript omicron: 24th and final Greek letter =Phoenician/Paleo-Hebrew 15th letter ayin “eye”; Egyptian “eye” 𓁹 jr (ḏ+r), mA (m + 3); rs; mAj; schp or some forms of Latin Q (17th letter; =Phoenician/Paleo-Hebrew pē, “mouth”, Egyptian 𓂋 “r” p(kh)ar).

A trader* who uses false balances, Who loves to overreach.†

* כְּנַעַן Canaan: “lowland”. 1. progenitor of the Phœnicians.

2. land west of Jordan river conquered by Israelites. 3. merchant, trader[5]

† wrong, violate, defraud, extort, oppress, get deceitfully[6]

* means weighed or shekel [7] †חַסִּיר (Chaldean): of weight, too light, deficient[8]

Today, the fourteenth (14) day of May in the year 2020 anno Domini (“In the year of (our) Lord”), is the seventy-second (72) anniversary of the Declaration of Independence of the nation state of Israel.[9]

An alternate form of capital Omega Ω resembles an underlined superscript omicron (15th Greek letter; =Phoenician/Paleo-Hebrew Ayin “eye”; Egyptian “eye” jr (ḏ+r), mA (m + 3); rs; mAj; schp) or some forms of Latin Q (17th letter; =Phoenician/Paleo-Hebrew Pē, “mouth”, Egyptian 𓁹 “r”).

On 14 May 1948, the thirty-third (33) President of the United States, thirty-three (33°) degree freemason Harry S. Truman, was the first world leader to officially recognise the rebirth of “the Jewish State,” eleven (da’at: ‘intimate’ ✡ “knowledge”) minutes later.[10]

On the midnight close of that day, the British Mandate for Palestine formally ended. Thus began the 1948 (or First) Israeli-Arab War.

If we see that Germany is winning the war we ought to help Russia and if Russia is winning we ought to help Germany and that way let them kill as many as possible… [11]

New York Times, June 24, 1941

Those with training in first aid will know the telltale signs that a living soul has deceased, or “passed on.” In absence of catastrophic damage or spilled lifeblood evidencing an act of violence, or fixed and dilated pupils suggesting that the “light of the eyes” has gone out, the most obvious is that their breast no longer rises and falls.

Yet another sign that their vital air ♦ or the “breath of life” has ceased “to go in and to go out” freely from the body’s “inner world” may be seen in the failure of their nostrils to “fog a mirror.”

“beautiful,” “good,” “perfect,” “fine,”

zero (0) in accounting, architecture, construction

In the Hebrew tongue, the word for this vital air ♦ is a feminine noun, נְשָׁמָהnᵉshâmâh, meaning breath, spirit, wind, the puff or pant of those who are angry; also intellect. It is derived from a primitive verb נָשַׁםnâsham, to puff or pant, used of a woman in labour; properly, to blow away, destroy.[12]

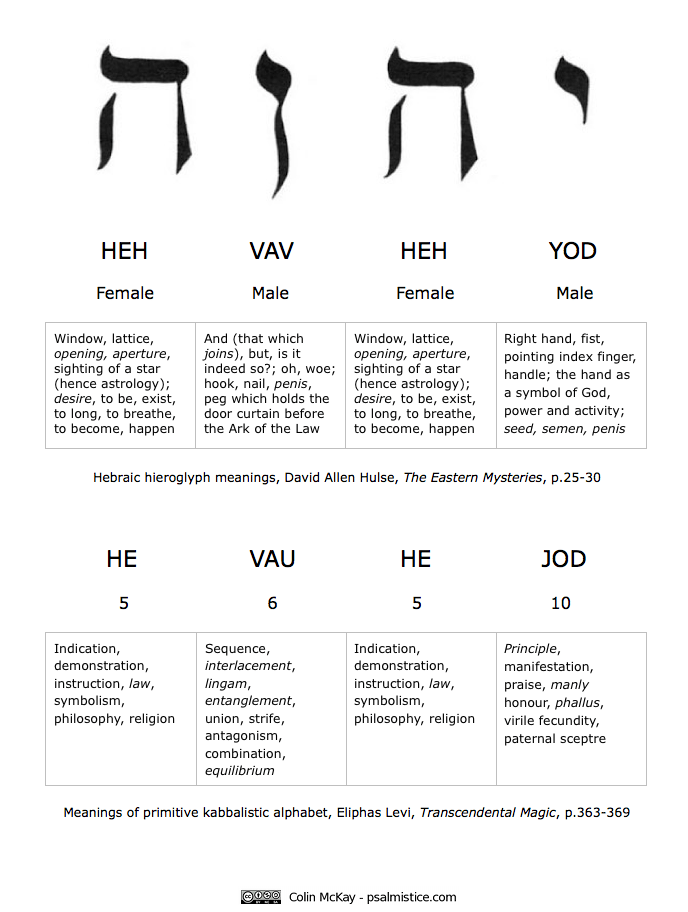

The Hebrew word for “living” and “life” is חַי ḥay, pronounced “chai.” It is derived from a root verb חָיָהchâyâh meaning to live; causatively, to sustain, preserve, restore, revive.[13] The letter hēה is a mater lectionis (“Mother of reading”); used as a suffix (as here) it denotes the feminine, the object to which men are directed. In Aramaic, the first alphabetical letter (אālap) is used to denote the feminine instead.

Chai (ḥay, “living”) in Ktav Ashurit (“Assyrian”) sacred script

There is another spelling for the Hebrew verb “to live” (חָיָה châyâh). Its letter forms and pronunciation differ only slightly. Indeed, the sole difference is a small vertical stroke downward, transforming the letter yod י into a vav ו. The word châvâh (חָוָה) means to breath, to live; properly, to breath out, to declare, to show, to make known.[14]

Stated another way, in the snake oiled salesman’s English tongue of ‘New Age’ gurus and Judeo-‘Christian’ televangelists, it means to ‘manifest’ … in particular, your ‘words of power.’

verb (transitive)

To show or demonstrateplainly;reveal

a. To record in a ship’s manifest.

b. To display or present a manifest of (cargo).

In Aramaic, the spoken tongue of common Judeans in antiquity—biblical ‘Hebrew’ being a sacred writing language reserved for the literate elite (c. 3%)[15]—this word is spelled חֲוָאchăvâʼ : the Mother letter hē ה replaced with an alephא. Its primary meaning is to show, interpret, explain, inform, tell, declare.[16]

An observant reader may notice that the Hebrew root חיהchayah (“to live, sustain, restore”) appears to contain the name of the biblical deity “Yah”,[17] prefixed by the eighth letter ḥet or chetח (“courtyard”). It is derived from the Egyptian hwt-(ḥut) 𓉗 (palace, temple or tomb), possibly via the Canaanite word ḥasir.

The deity’s name “Yah” is composed of the fifth (and Mother) letter hēה and the tenth letter yodי . It is derived from a Canaanite glyph for the word yad “hand”. This derives from an Egyptian hieroglyph for the uniliteral sign ayinꜥ “eye” (whence ancient Greek ninth letter iota, Latin and English “i”), depicting a forearm with palm facing up 𓂝 .[18]

The broad, broad realms of Lycurgus . . . where stretches icy Rhodope to Haemus with its shades, and sacred Hebrus drives his headlong waters forth.

— Ovid, Heroides 2. 111 ff.

Hebros (Hebrus), you flow, the most beautiful of rivers, past Ainos (Aenus) into the turbid sea, surging through the land of Thrake (Thrace)* . . .

— Alcaeus, Fragment 45a

* From Latin Thrācia, from Ancient Greek Θρᾴκη(Thrā́ikē), from Θρᾷξ(Thrâix, “Thracian”), from base of θράσσω(thrássō, “to trouble, stir”) and -ιξ(-ix), compare Φοῖνιξ(Phoînix, “Phoenician”).

In ancient Egyptian culture, there developed over three thousand years a highly sophisticated system of funeral rites. The renowned English Egyptologist, Orientalist, philologist and British Museum curator, Sir E.A. Wallis Budge, described these as consisting of “spells and incantations, hymns and litanies, magical formulae and names, words of power and prayers, and they are found cut or painted on walls of pyramids and tombs, and painted on coffins and sarcophagi and rolls of papyri.”[20]

No small injustice is done these by our lamentably brief summary. Time set aside for their study is commended as time well spent, and this not only for the appreciation of a culture whose extraordinary achievements have enthralled and—as we will see—shaped and influenced humankind for millennia. For in addition, the knowledge gained is sure to re-cast the brazenly deceitful claims of some to a divinely ordained “chosen”-ness, exclusivity, originality, superiority, a “promised” inheritance of “eternal” Levantine land rights, and a global ‘utopian’ slave theocracy ruled from Uru-šalim*, in a revelatory new light.

* from West Semitic yrw, “to found, to lay a cornerstone”, and Shalim, a Canaanite god of the setting sun and the Underworld. He is one half of a pair of deities—Dioskouroi, a la the Greco-Roman twins Castor and Pollux—named šḥr w šlm (Shahar and Shalim). Known as ‘the Devourers’ for their having insatiable appetites, “(one) lip to the earth and (one) lip to the heaven,” they represent the liminal (ambiguous, transformative) horned planet Venus ♀ in its opposite pair, dawn and twilight aspects: the Beginning and End of the life-light of day (ym ים “yôm”)†, the Morning and Evening Star. The name Š-L-M is the triconsonantal root of many semitic words and names, including Solomon, the biblical paragon of wisdom, and ruler of demons. It has a base meaning of “completion” (in the sense of death), sunset, well-being, safe, and wholeness, whence the greetings in Hebrew (“shālôm”) and Arabic (“salām”) — peace.[21]

† ymים “day”: Canaanite pictograph of the hand (yad) representing work, and another of rippling (troubled, stirred) water (מים mayim). It means “working water”.[22]

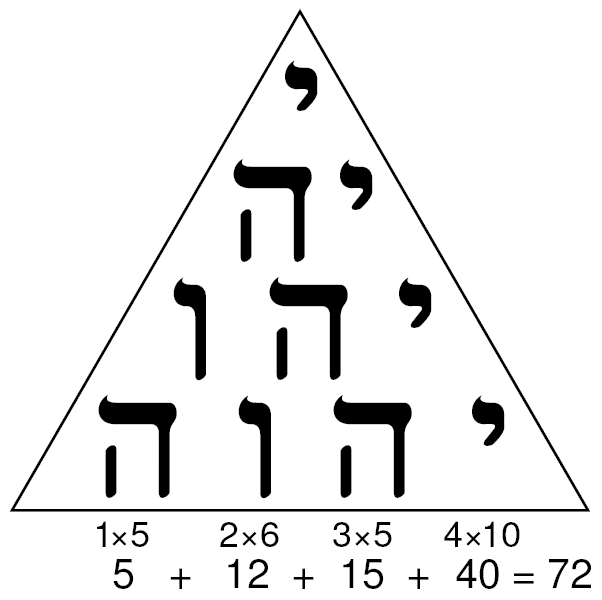

“Ten million” (yod ) plus “five more” (Mother letterhē ,

and Egyptian godḤeḥ 𓁨 “million”=“infinity”, “flood”)

=“Yah”, proper name of Canaanite copper ♀ serpent deity[17]

=Fifteen (samekh ): serpent spine, the Devil &/or Lust

In gematria, no. 15 is written with the ninth and sixth letters

(ṭēt + vav, 9+6) to avoid spelling the ‘ineffable name’

“Vesper. I do hope you gave your parents hell for that.”

Sorry for our length.

Also, for our volume and weight. Hopefully we are still able to command your attention.

We may have neglected to mention that the Egyptian royal cubit (meh niswt), a unit of length measurement, was represented using the same glyph as that adopted by the Canaanites for yad (“hand”), but with the palm turned down 𓂣 . Each ‘rod’ was seven (7) palms (20.61 to 20.83 in) long.[23]

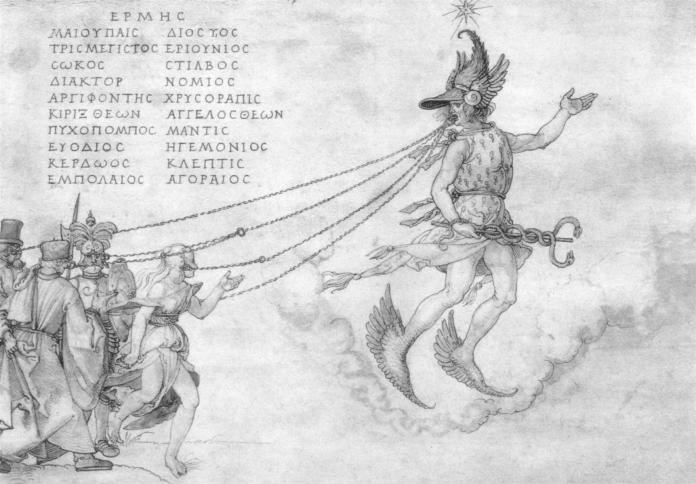

In order to reach the Kingdom of Osiris, ruler of the Underworld in one’s afterlife, the Egyptian petitioner trusted in the cleverness of the moon-god, Thoth (later, Greek Hermes ☿ Roman Mercury), ruler of wisdom, writing, measurement, arts, sciences, philosophy, magic and trickery; an aggressive, overtly virile dog-faced baboon or ibis-headed deity, with the power of divine boundary-crossing.

Book I, XIV, Hieroglyphics of Horapollo, tr. Alexander Turner Cory, (1840)

To denote the moon, or the habitable world, or letters, or a priest, or anger, or swimming, they pourtray a CYNOCEPHALUS. And they symbolise the moon by it, because the animal has a kind of sympathy with it at its conjunction with the god. For at the exact instant of the conjunction of the moon with the sun, when the moon becomes unillumined, then the male Cynocephalus neither sees, nor eats, but is bowed down to the earth with grief, as if lamenting the ravishment of the moon: and the female also, in addition to its being unable to see, and being afflicted in the same manner as the male, ex genitalibus sanguinem emittit [Latin: “emits blood from the genital organ”]: hence even to this day cynocephali are brought up in the temples, in order that from them may be ascertained the exact instant of the conjunction* of the sun and moon.

The animal is moreover consecrated to Hermes [Thoth], the patron of all letters. And they denote by it a priest, because by nature the cynocephalus does not eat fish, nor even any food that is fishy, like the priests. And it is born circumcised, which circumcision the priests also adopt. And they denote by it anger, because this animal is both exceedingly passionate and choleric beyond others:—and swimming, because other animals by swimming appear dirty, but this alone swims to whatever spot it intends to reach, and is in no respect affected with dirt.[24]

This slideshow requires JavaScript.

Before we continue, a digression, for words of caution.

This essayis written with a conscious intention. As indeed will others that, for considerations of length, weight, and volume[25] (pointed puns intended),must, God willing, necessarily follow. Our aim is to shatter the tempered glass foundational ceiling of main-streamed theologico-historical beliefs. Cryptic, pointed, paradoxical, mixed metaphors intended. Many have been promoted for millennia as truths beyond question.

There is a white irony in this.

Our intention is analogous to that of the reviled dukhifat or shamir, the “rock-splitter” of ancient mythology, and Jewish demonology: trying to reach its children, trapped under a plane of translucence by a cunning thief. Indeed, this very subject is one of many on which we will have reason to learn rather a lot more in future.

Solomon said to him: I need nothing from you. I want to build the Temple and I need the shamir for this. Ashmedai [Prince of demons] said to him: The shamir was not given to me, but it was given to the angelic minister of the sea. And he gives it only to the wild rooster, also known as the dukhifat or the hoopoe, whom he trusts by the force of his oath to return it.[26]

The shamir was the seventh of the ten marvels created in the evening twilight of the first Friday, and it was followed, significantly enough, by the creation of writing, the stylus, and the two tables of stone.[27]

Hearts, Chalices or Cups ♥ Spades, Swords or Athamés ♠

Clubs, Rods, Staves or Wands ♣

Diamonds, Pentacles, Coins, Discs or Rings ♦

“You Know My Name” sung seven (7 zayin) times in finale,

eight (8 ḥet, chet) times in total.

And while [Jesus] yet spake, lo, Judas, one of the twelve, came, and with him a great multitude with swords ♠ and staves* ♣, from the chief priests and elders of the people.

* Ancient Greek ξύλον xýlon: ‘wood’; a cudgel or club; a beam or cross to which a prisoner is bound with bands or thongs 𓋹 ; fetters (‘bonds’, ‘stocks’) made from ‘wood’; bench, table, espec. a money-changer’s table.[29]

This slideshow requires JavaScript.

“undercurrent of sarcasm in her voice,” “Her beauty’s a problem,”

“any woman with half a brain,” “overcompensates by wearing

slightly masculine clothing,” “a somewhat prickly demeanour.”

Tarot (“rō′tāt”) Major Arcana traditional trump no.

8. Justice variable with 11. Strength

(pun intended) since late 19th century due ‘British’ influence:

Rider-Waite-Smith and Hermetic Order of the Golden Dawn

But not today.

In earnest and empathetic awareness of the risk of causing offence with informing criticism, our hope is that the reader will be drawn to carefully and prayerfully contemplate the material presented, with this thought held in front of mind.

However troubling you may find the content following, know this. There is a silver chord of pure, inspirational, joyous, divine truth, deeply buried, it must be said, and yet running still, through a truly colossal mountain of malodorous lies.

In seeking to shatter the frosted glass pane of word magicians—the thieves and concealers of truth—it is our intention to liberate the truth, in the bright light of day. It is hoped that others will find these and latterly elaborated discoveries to be faith affirming, rather than the opposite.

In the longue durée, despite our often ignore-ant, foolish, and yes, evil ideas and actions, it is evident that God exists. A Supreme, knowable power who, with a readily perceptible character of infinite Patience, softly and silently laboursto re-form, or re-shape, good outcomes (unity, harmony, order, peace, joy) from our self-created evil ones (division, disharmony, disorder, war, grief). And in this comprehension, we will perceive that the doctrine of an afterlife—of regeneration, or rebirth—rings true.

This we will also see in the progressive revelation of pathologically obsessive, narcissistic efforts to muddy our waters—puns intended—and so obscure this truth; stealing and hiding the keys to eternal life.

The concept of rebirth has appeared in many permutations and glosses throughout human history. The secret of its fruition is in a clear recognition, an understanding, and a humble acceptance, of whose power, judgement, wisdom, and free will choice it is that makes an individual’s regeneration, or re-form-ation possible.

A further re-cognition too, is necessary. In the long run, liars and cheats never prosper.

Contrary to all the sophistication and complexity of ancient Egyptian through Jewish Cabalist letter, “name” and number magic formulae—and notwithstanding aid sought from ‘good’ demons—no human intellect can outwit a Supreme Intellect. It is perhaps the ultimate manifestation of egotistical and foolhardy self-delusion to think oneself smart enough to deceive the Ultimate Judge with ‘magic’ wordplay. Especially when the destiny of one’s soul hangs in the balance.

For both Yeshua [Jesus], who sets people apart for God, and the ones being set apart have a common origin — this is why he is not ashamed to call them brothers when he says,

“I will proclaim your name to my brothers; in the midst of the congregation I will sing your praise.”[a]

“Here I am, along with the children God has given me.”[c]

Therefore, since the children share a common physical nature as human beings, he became like them and shared that same human nature; so that by his death he might render ineffective the one who had power over death (that is, the Adversary) and thus set free those who had been in bondage all their lives because of their fear of death.

Alas, the religion of “God’s chosen people” has progressed not one whit—nor iota (but I repeat myself)—from ancient Egyptian hubris.

Let us consider the words of an exemplary case in point: the Kabbalist Who Would Be King of a New Jewish Monarchy in Israel. A rabbi described by a former student as a paradox: “On the one hand he is a brilliant thinker, an innovator, has a great sense of humor, wide knowledge of Kabbalah as well as the sciences. On the other hand, this person disseminates racist and violent preaching.” This ‘brilliant’ mind has yielded such pearls of wisdom and holiness as “the best goy is a dead one,” and “There is something infinitely more holy and unique about Jewish life than non-Jewish life”:[31]

The unknowable, superconscious head [Hebrew letter reish ר “head”, from the Egyptian hieroglyph 𓁶 ] of the first day of Rosh HaShanah is the secret of “‘for My thoughts are not your thoughts, neither are your ways My ways,’ says G-d, ‘for as the heavens are higher than the earth, so are My ways higher than your ways, and My thoughts than your thoughts.’” These two verses precede the verse: “Seek G-d while He may be found, call upon Him while He is near…”

This is the secret of “lift up the head of the Children of Israel.” The root to lift up in Hebrew, נָשָׂ֣א *, means the power to bearthe opposites, the divine paradox of the unknowable head.[32]

This is the first of many examples of “The Power of Ambiguity”[33]—to wit, multiple meanings, often diametrically opposed—that is all-pervasive in the Jewish peoples’ supposedly ‘holy’ tongue; a brazen lie which, we will discover, lies at root of more lies than the Edomite and Israelite copper serpent deity’s “sand of the sea” promise.

* נָשָׂ֣א nâsâʼ he lifted, raised, carried, carried off, married, swept away, destroyed, forgave, pardoned; also he claimed a debt, and (Hiphil) he deceived, beguiled[34]

cf. נָסָהnâśâ’, nâsâh to lift up, bear up; Arabic (to occur, esp. to arise in the mind) نشا to smell, to try by the smell, to try, to prove anyone. 1 Kings 10:1, “the queen of Sheba came, לְנַסֹּתוֹ בְּחִידוֹת to prove him with hard questions;” to examine the wisdom of Solomon, 2 Chronicles 9:1.[35]

The letters “n” (נ nun) and “s” (סsamekh,alternates with שׂ shin) derive from Egyptian hieroglyphs of a resting snake (cobra), and the spinal column of the supreme deity.[36] In Jewish esotericism, these are associated with the reversal or inversion of nature’s laws. In occult sex magic ritual, and bank credebt ‘lending’ by double entry bookkeeping, they are associated with the ‘art’ of stealing the seed of the woman.

“As to the serpent cobra, it is the color of sand. If it bites someone, he will feel pain in one half [of his body] where he has not been bitten and will not feel pain in the half that has been wounded. [..] This is a manifestation of Sēth. The bitten does not die.[37]

Set on a late New Kingdom relief from Karnak

Set spears Apep, the dark chaos deity

In early Egyptian mythology, Set was a god seen in a positive light: lord of the red desert land, accompanying Rā (the Sun-god) on his nightly journey through the Underworld to repel the dark chaos serpent, Apep. Due to his adoption as the supreme god of the Hyksos or Shepherd-Kings—“asiatic” invaders who ruled lower Egypt in the Second Intermediate period—following the expulsion of the “asiatics” into Judea the Egyptians recast Set (pun intended) in a wholly negative light. He became the desert storm god of envy, trickery, chaos, destruction, disorder, who had killed his own brother Osiris, hoping to usurp the throne. Osiris’ death was avenged in combat with Horus, the son of Osiris. Thanks to the ‘cleverness’ of Thoth in the Judgement Hall of the Gods, Osiris became lord of the Underworld. Significantly, and worthy of note for viewers of Casino Royale, Set was defeated only after blinding Horus in one eye.

Endless volumes have been written on the nature and identity of “Jewishness”. In express context of the rebirth of “the Jewish State”, it is inarguable—by any person having even a distant relationship with honesty and objectivity—that the Jewish religion has played, and continues to play, directly and/or indirectly, a fundamental, essential role in the history, psychology, and behaviour, of all persons self-identifying as “Jews,” whether overtly or covertly, with good intention or ill.

To speak plainly and simply: in absence of the Jewish religion, with its claims to a ‘divine’ historicity, and a messianic ‘utopian’ futurity, there would be no Jewish identity.

As we will discover, the supposedly ‘divine’ history of Judaism is a colossal mountain of lies. From its Genesis onward.

The Hebrew bible is a classic example of history being written and re-written by the ‘winners’. The line “And I will replace you” in the Casino Royale title track could not be more apt.

Seen in holistic view, the entire biblical narrative pivots around the tales of brothers—often twins—in lineages purportedly tracing back to the first human parents. In the signature examples, one brother is clearly portrayed as envious, lying, cheating, deceiving, thieving, murdering; stopping at nothing in the quest to gain an exclusive monopoly on ‘divine’, and more specifically, hereditary preference. Revealingly, the most famous example depicts a younger twin conniving with his similarly dishonest Mother to trick their old Blind Father, and cheat the heir of his inheritance rights.

“And I will replace you.”

These fraternal conflicts, and the no conscience, amoral depravities portrayed, are arbitrarily disregarded, or worse, given ‘divine’ sanction by the alleged “blessings” of a deity clearly projected in its authors’ own image, and after their likeness. Indeed, the titular patriarchal hero and namesake of the “Jewish State” features as the exemplar of a demon prince masqueraded as an angel of light: Jacob (יַעֲקֹב “heel-catcher”, i.e., usurper, layer of snares), renamed Israel (יִשְׂרָאֵל “contender”).

So let us not mince words.

Judaism is the religion of the obsessive compulsive. The psychotic. The Cluster B and C personality disorder. The histrionic. The borderline psychotic. The narcissist. The psychopath.

It is the religion of the “homoerotic,” “misogynistic,” sexuality-obsessed, paedophilic ‘sage’.[38][39]

It is a religion that equates the Jewish penis and the tongue: the ‘divine’ organs of ‘creation’.[40]

Judaism is the religion of doublethink. In the words of George Orwell, a “vast system of mental cheating.”[41]

The God of Judaism is an “oxymoronic ‘male androgyne'”: a male form of supposedly formless deity, possessing all characteristics of, and having dominion over, both the female and male genders.[42]

For Judaism, all knowable and unknowable reality is divided into a binary: male and female, good and evil. This, an essentially gnostictheosophical worldview is contradicted by another non falsifiable abstraction—otherwise known as a fantasy or delusion—and a fundamental predilection of Judaism: the paradoxical insistence that all manifestations of reality, all forces, good and evil, originate in the one source, the Divine Intellect.

It would seem that the (little “d”) ‘divine’ intellects of the ‘Sages’ are unable—or perhaps, simply un-willing—to recognise, understand, and accept, that darkness and light, good and evil are not equal opposite forces, or ‘powers’. They are not +1 | -1 numbers on a double entry bookkeeping ledger.

Dark is the result of an absence, obstruction, or rejection of Light.

Evil is the result of an absence, obstruction, or rejection of Good.

The aspiration of Judaism is to become “like God”: to wit, the kind of “God” that its ‘Sages’ say is “God”. A ‘pure’ intellect. A “superconscious” Creator of all paradoxes. All ‘opposites’. All unreason, and illogic. All circularity. All stupidity. All chaos, and confusion. All conflict, disorder, anger, anomie, nihilism, and death.

In other words, the purpose of Judaism is to become as its ‘Sages’ imagine God to be: a ‘divine’ doublethink-er.

But not in the next world. In “the World to Come” right here.

Goyim were born only to serve us. Without that, they have no place in the world; only to serve the People of Israel. Why are gentiles needed? They will work, they will plow, they will reap. We will sit like an effendi and eat.

— Chief Sephardi Rabbi of Israel, Ovadia Yosef [43]

[The] Kabbalists in Spain cultivated a violent, demonic form of magical Kabbalah intended to destroy the prevailing historical and religious order, including [especially – CM] Christianity, for the sake of bringing the Messiah.

As Rabbi Ginzburg, The Kabbalist Who Would Be King explains:

In Torah, both reward and punishment have the same ultimate aim—the rectification of the soul to merit to receive G-d’s light to the fullest extent.

Reward and punishment imply that a man is free to choose between good and evil. [..] The Rambam (Maimonides), in particular, places great stress upon free choice as being fundamental to Jewish faith. According to the Rambam, the World to Come, the time of reward, is a completely spiritual world, one of souls without bodies. On this point the Ramban (Nachmanides) disagrees and argues that since complete freedom of choice exists only in our physical world, the ultimate rectification of reality—the reward of the World to Come—will also be on the physical plane. Kabbalah and Chassidut support the opinion of the Ramban.[45]

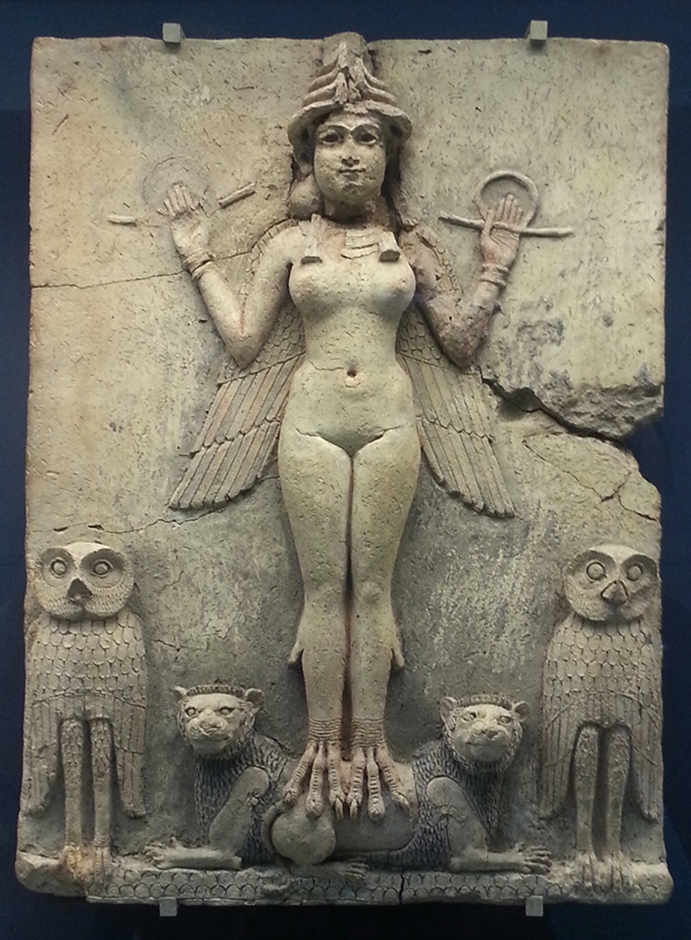

The Egyptians believed Thoth, the lord of the Balance, to be not only the heart and mind of the Creator, but his clever tongue as well:

…he at all times voiced the will of the great god, and spoke the words which commanded every being and thing in heaven and in earth to come into existence. His words were almighty and once uttered, never remained without effect. He framed the laws by which heaven, earth and all the heavenly bodies are maintained; he ordered the courses of the sun, moon, and stars; he invented drawing, design and the arts; the letters of the alphabet and the art of writing; and the science of mathematics. At a very early period he was called the “scribe (or secretary) of the Great Company of the Gods,” and as he kept the celestial register of the words and deeds of men, he was regarded by many generations of Egyptians as the “Recording Angel.” He was the inventor of physical and moral Law and became the personification of JUSTICE; and as the Companies of the Gods of Heaven, and Earth, and the Other World appointed him to “weigh the words and deeds” of men. His verdicts were unalterable, and he became more powerful in the Other World than Osiris himself. Osiris owed his triumph over Set in the Great Judgment Hall of the Gods entirely to the skill of Thoth of the “wise mouth” as an Advocate, and to his influence with the gods in heaven. And every follower of Osiris relied upon the advocacy of Thoth to secure his acquittal on the Day of Judgment, and to procure for him an everlasting habitation in the Kingdom of Osiris.[46]

Spells and other magical texts written by Thoth for the benefit of the deceased were called “Chapters of the Coming Forth by (or, into) the Day.” These compositions were greatly reverenced, as they would “make a man victorious upon earth and in the Other World; it would ensure him a safe and free passage through the Tuat (Underworld); it would allow him to go in and to go out, and to take at any time any form he pleased; it would make his soul to flourish, and would prevent him from dying the [second] death.”[47]

This slideshow requires JavaScript.

In great papyri of the Book of the Dead such as those of Nebseni, Nu, Ani, Hunefer, etc., the Last Judgment, or the “Great Reckoning,” is made the most prominent scene in the whole work… The most complete form of it is given in the Papyrus of Ani… Since the heart was considered to be the seat of all will, emotion, feeling, reason and intelligence, Ani’s heart is seen in one pan of the Balance, and in the other is the feather 𓆄 , symbolic of truth and righteousness.

While his heart lies in the Balance, Ani repeats the words from the Book of the Dead quoted at top this essay.

Then Thoth, the Judge of Truth, of the Great Company of the Gods who are in the presence of Osiris, saith to the gods, “Hearken ye to this word: In very truth the heart of Osiris hath been weighed, and his soul hath borne testimony concerning him; according to the Great Balance his case is truth (i.e., just). No wickedness hath been found in him. He did not filch offerings from the temples. He did not act crookedly, and he did not vilify folk when he was on earth.”

And the Great Company of the Gods say to Thoth:

“This that cometh forth from thy mouth of truth is confirmed (?) The Osiris, the scribe Ani, true of voice, hath testified. He hath not sinned and [his name] doth not stink before us; Amemit (i.e., the Eater of the Dead) shall not have the mastery over him. Let there be given unto him offerings of food and an appearance before Osiris, and an abiding homestead in the Field of Offerings as unto the Followers of Horus.”

In all the copies of the Book of the Dead the deceased is always called “Osiris,” and as it was always assumed that those for whom they were written would be found innocent when weighed in the Great Balance, the words “true of voice,” which were equivalent in meaning to “innocent and acquitted,” were always written after their names. It may be noted in passing that when Ani’s heart was weighed against Truth, the beam of the Great Balance remained perfectly horizontal. This suggests that the gods did not expect the heart of the deceased to “kick the beam,” but were quite satisfied if it exactly counterbalanced Truth. They demanded the fulfilment of the Law and nothing more, and were content to bestow immortality upon the man on whom Thoth’s verdict was “he hath done no evil.”[48]

The Last Judgment or “Great Reckoning” (Papyri of Ani)

On successfully passing the Weighing of the Scales, and presentation before Osiris, the deceased “comes forth by day” as a living god in the Underworld (dwꜣtDuat); the abode of the sun that has set:

𓇽

Rā sets as Osiris with all the splendour of the Glorified and of the gods of the Amentafor he is the one, the marvellous in the Tuat, the exalted soul in the Netherworld, Unneferu who exists for ever and eternally.

Amenta: the Underworld, horizon where the sun sets, west bank of the Nile, place of the dead.

Look at me, ye blessed ones, divine guides in the Tuat; grant that I may receive thy glory, that I may shine like the god of mysteries [..]I am the heirof Osiris, I receive the nemmes in the Tuat.

Look at me, I shine like one who proceeds from you, I become like him who (praises) his father, and who extols him.

Look at me, rejoice in me, grant that I may be exalted, that I may become like him who destroys his forms; open the way to my soul, set me on your pedestals; grant that I may rest in the good Amenta, show me my dwelling in the midst of you, open for me your ways, unfasten the bolts.

I am the favouriteof Ra; I am the mysterious Bennu who enters in peace in the Tuat and goes out of Nut in peace.

I am the lord of the thrones above, traversing the horizon in the train of Ra; the offerings for me are in the sky in the field of Ra, and my portion on earth in the garden of Aarru; I journey in the Tuat like Ra; I weigh the words like Thoth, I march as I will, I hasten in my course like Sahu the mysterious one, and I am born as the twogods.[49]

“I”.

“I” “i” “i” “i” “i”.

Mmmm .

Good luck with that, moonshine

You may not get any more sympathisers if you draw a crook hand.

******************

REFERENCES

Omega/ˈoʊmɪɡə,oʊˈmɛɡə/ (capital: Ω, lowercase: ω; Greek ὦ, later ὦ μέγα, Modern Greek ωμέγα) is the 24th and last letter of the Greek alphabet. In the Greek numeric system/Isopsephy (Gematria), it has a value of 800. The word literally means “great O” (ō mega, mega meaning “great”), as opposed to Ο ο omicron, which means “little O” (o mikron, micron meaning “little”).

[1] Estoppel is a judicial device in common law legal systems to prevent or “estop” a person from making assertions or from going back on their word. Estoppel may prevent someone from bringing a particular claim. The Legal Dictionary describes estoppel as “a legal principle that bars a party from denying or alleging a certain fact owing to that party’s own previous conduct, allegation, or denial.”

The verb estop comes from Middle English estoppen, borrowed from Old French estop(p)er, estouper, presumably from Vulgar Latin *stuppāre ‘to stop up with caulk, tow’ [coarse broken flax, Middle English, possibly from Old English tow-, spinning (in towcræft, spinning craft, spinning)], from Latin stuppa, ‘broken flax’, from Ancient Greek stuppē, ‘broken flax’.

Compare Matthew 12:20, cit. Isaiah 42:3:

A bruised reed [by impl. a pen] shall he not break, and smoking flax shall he not quench: he shall bring forth judgment unto truth.

[2] See (e.g.) Book of Tobit (chapters 6-8), “13” secret ingredients of Temple incense. See Gideon Bohak, Ancient Jewish Magic: A History (New York: Cambridge University Press 2008), p.89 on story in Book of Tobit, “probably written in the fourth or third century bce, perhaps by a Babylonian Jew”:

The technique itself consists of fumigating the heart and liver of a certain fish from the Tigris river (the fish’s gall also serves to heal Tobit’s eyes, but not by way of exorcism),* and Raphael promises the young Tobias that this will drive away any demon or evil spirit and keep them away forever (6.8, 16–17). Before the consummation of his marriage with Sarah, Tobias indeed places the fish’s liver and heart on an incense burner, and the resulting odors drive the evil Ashmedai all the way from Persian Ecbatana to Upper Egypt, where Raphael quickly binds him up (8.2–3).

*For Babylonian precedents, see von Soden 1966

[3] Sir Peter Le Page Renouf and Prof. E. Naville, The Egyptian Book of the Dead: Translation and Commentary (London: Harrison and Sons 1904), p.75

[4] Maria Carmela Betrò, Hieroglyphics: The Writings of Ancient Egypt (New York: Abbeville Press 1996), p. 179 Sandal –

𓋸 This hieroglyph represents a very simple form of sandal: a sole with two strips of leather or other material to keep the foot in place. They are present in tombs from as early as the First Dynasty at Abydos (the beginning of the third millennium B.C.). [..] The cosmetic palette of King Narmer, dating from the end of the fourth millennium B.C., shows a high functionary (perhaps even a vizier) immediately behind the king, carrying the king’s sandals. Shoes at this time were a status symbol: the wearing of sandals was an unequivocable indication of rank. In the Old Kingdom, sandals were still the prerogative of kings, priests, and high dignitiaries: everyone else walked unshod. [..] During the Middle Kingdom, sandals became quite common: for example, they were given to the members of expeditions about to cross the desert.

Narmer’s Palette from Hierakonpolis (end 4th millennium BC). Cairo, Egyptian Museum (source: M.C. Betrò, Hieroglyphics 1996)

p. 155 The Otherworld –

𓇽 A star (dwꜣt, morning, place where the sun is born) in a circle: this is the symbol for the otherworld. Initially in the Pyramid Texts, this sign stood for the place in the sky where the sun and the stars reappeared after having been invisible; then it began to represent the otherworld, whether celestial or subterranean. [..] When the destiny of the deceased began to be associated with the symbolic death of the god Osiris, the otherworld began to be envisioned as an underground space with an intricate and detailed geography. The dead moved through this subterranean otherworld with the help of funerary rites and the so-called “guides” to the otherworld… The circle of the Duat is a symbol of cyclical rebirth. Like other Egyptian metaphors for life in the afterworld, it is a closed internal space that is naturally associated with the image of the female womb, the point of departure and hoped-for destination.

For the Testament of Solomon (F.C. Conybeare transl.) see esotericarchives.com (online)

[5] Canaan (כְּנַעַן), Brown-Driver-Briggs (BDB) Hebrew and English Lexicon (online)

[6] ‛âshaq (עָשַׁק), Brown-Driver-Briggs (BDB) Hebrew and English Lexicon (online)

[7] Tekel (תְּקֵל), Brown-Driver-Briggs (BDB) Hebrew and English Lexicon (online)

[8] chassı̂yr (חַסִּיר), Brown-Driver-Briggs (BDB) Hebrew and English Lexicon (online)

[9] The Declaration of Independence, archives.gov.il (retrieved 10 May 2020)

[10] Recognition of Israel, Harry S. Truman Presidential Library and Museum, truman.gov (retrieved 10 May 2020)

[11] Harry S. Truman: Decisive President, New York Times archives, (retrieved 10 May 2020)

[15] M.O. Wise, Language and Literacy in Roman Judaea: A Study of the Bar Kokhba Documents (New York: Yale University Press, 2015). Meir Bar-Ilan speculated c. 3% Jewish literacy in antiquity.

[17] Yah, proper name of God, for biblical refs see Gesenius’ Hebrew-Chaldee Lexicon (online)

[18] Brian Colless (The Origin of the Alphabet, Antiguo Oriente, volumen 12, 2014, pp. 71–104, a critical review of Orly Goldwasser theory)

[19] Herodotus, The Histories Book V (A.D. Godley, Ed.), perseus.tufts.edu (retrieved 13 May 2020)

[20] E.A.W. Budge, The Ancient Egyptian Book of the Dead (New York: Quarto Publishing Group 2016), p.3

[21] Shalem (Deity), The Anchor Bible Dictionary (online, retrieved 13 May 2020). Compare Karel Van Der Toorn, Bob Becking, Pieter W. Van Der Horst, Dictionary of Deities and Demons in the Bible (xxx: 1999 Second Edition), pp. 100 and 109-11:—

ASHERAH: Apart from mention in sacrificial and pantheon lists, the goddess also appears in two theogonic texts, KTU 1.12 i and 1.23, the former describing the birth of ‘the Devourers‘ to the handmaids of Athirat and Yarihu, the latter describing two wives of EI (seemingly Athirat and perhaps Shapsh) who consummate their marriage with him, and give birth to →Shahar and →Shalem, the →Dioskouroi. These texts have a bearing on several biblical traditions, such as Gen 16, 19:30-38, Ps 8 etc. (WYAlT 1993). The goddess’ name appears in the longer title rbt aṯrt ym, meaning perhaps ‘the Great Lady who walks on the Sea‘ (the name therefore apparently understood as ‘Walker’) . . .

This slideshow requires JavaScript.

ASTARTE: The divine name Astarte is found in the following forms: Ug ‘ṯtrt (‘Athtart[u]’); Phoen ‘štrt (‘Ashtart’); Heb ‘Aštoret (singular); Aštarot (generally construed as plural); Eg variously ‘sṯrt, ‘sṯrṯ, istrt; Gk Astarte. It is the feminine form of the masculine ‘ttr (‘Athtar’. ‘Ashlar’) and this in turn occurs, though as the name of a goddess. as Akkadian→Ishtar. The Akkadian Aš–tar-[tum?] is used of her (AGE 330). The etymology remains obscure. It is probably, in the masculine form, the name of the planet Venus, then extended to the feminine as well (cf. A.S. YAHUDA, JRAS 8 [1946] 174-178). [..] Both god and goddess are probably, but not certainly, to be seen as the deified Venus (HEIMPEL 1982: 13-14). This is indeed the case, since if the morning star is the male deity (cf. Isa 14: 12), then the goddess would be the evening star: as she is in Greek tradition. (The two appearances of Venus are also probably to be seen as deified, cf. →Shahar and →Shalem.)

Egypt. Astarte is mentioned a number of times in texts from Egypt. In one instance, her name is written ʼntrt. Even if this is simply a misspelling, as LECLANT (1960:6 n.2) suggests, it is still ‘revealing’ (but cf. ANET 201a n. 16). In the Contendings of Horus and Seth (iii 4), →Seth is given Anat and Astarte. the daughters of →Re, as wives. This is a mythologisation of the importing of Semitic deities into Egypt under the Hyksos and later, and the New Kingdom fashion for the goddesses in particular. Seth and Baal were identified. [..] Anat and Astarte are described in a New Kingdom text (Harris magical papyrus iii 5 in: PRITCHARD (1943:79]) as “the two great goddesses who were pregnant but did not bear“, on which basis ALBRIGHT (1956:75) concludes that they are “perennially fruitful without ever losing virginity”. He also asserts that “sex was their primary function”. Both assumptions are questionable, not to say mutually incompatible! As wives of Seth, who rapes rather than makes love to them, their fruitless conceptions are an extension of his symbolism as the god of disorder, rather than qualities of their own. In the fragmentary ‘Astarte papyrus’ (ANET 17-18; see HELCK 1983) the goddess is the daughter of →Ptah and is demanded by the →Sea in marriage.

[22] ym ים “day”, Ancient Hebrew Lexicon (online, retrieved 12 May 2020)

[23] Cubit#Ancient_Egyptian_royal_cubit, Wikipedia (online, retrieved 12 May 2020)

[24] Alexander Turner Cory, The Hieroglyphics of Horapollo Nilous (1840), (online, retrieved 13 May 2020)

[25] Sefer HaChinukh (“Book of Education”) 259 (Spain c.1255 – c.1285 AD):

The commandment of having just scales, weights and measures: To have just scales, weights and measures and to be very careful about them, as it is stated (Leviticus 19:36), “You shall have just scales, just weights, a just eiphah, and a just hin.” And the language of Sifra, Kedoshim, Chapter 8:7 [is] “‘Just weights’ – justify the scales precisely” – meaning to say, that the scales be righteous. And the matter is well-known regarding scales that there are important adjustments to make, as it is possible to do many types of falsehood with them. “‘Just weights’ – justify the weights precisely” – also with weights, it is also possible to do many types of falsehood, and similar to that which they, may their memory be blessed, said (Bava Metzia 61b), “I will repay in the future anyone who submersed his weights in salt.”

Rav Yeimar said to Rav Ashi: Why do I need the prohibition that the Merciful One wrote with regard to weights: “You shall do no unrighteousness in judgment, in measure, in weight, or in volume” (Leviticus 19:35)? It is merely another form of robbery. Rav Ashi said to him: It is referring to a seller who buries his weights in salt, in order to lighten them.

The Sages taught: The verse states: “You shall do no unrighteousness in judgment, in measure, in weight, or in volume [uvamesura]” (Leviticus 19:35). “In measure”; this is referring to the measurement of land, e.g., this means that in a case where two people are dividing their jointly owned field, one may not measure the land to be given to one during the summer and measure the land to be given to the other during the rainy season, because the length of the measuring cord is affected by the weather conditions. “In weight”; this is referring to the fact that he may not bury his measuring weights in salt. And “in volume”; this teaches that one may not froth the liquid one is selling, creating the impression that there is more liquid in the vessel than there actually is.

[26] Babylonian Talmud Gittin 68a, William Davidson translation (online, retrieved 8 May 2020)

[27] Shamir, Jewish Encyclopedia 1906, Wilhelm Blacher, Ludwig Blau (online, retrieved 11 May 2020) —

This last account is Babylonian in origin, and both language and content prove that it was a legend of the people rather than a tradition of the schools, as is the case with the stories mentioned above. There were, however, learned circles in Palestine which refused to credit the use of the shamir by Solomon (Mek., Yitro, end). Others, however, believed that Solomon employed it in the building of his palace, but not in the construction of the Temple, evidently taking exception to the magical element suggested by a leaden box as a place of concealment, for in magic brass is used to break enchantment and to drive away demons (Soṭah 48b; Yer. Soṭah 24b).

[28] Matthew 26:47, The Holy Bible King James transl., (online, retrieved 12 May 2020)

[29] xýlon, Liddell-Scott-Jones and Thayer’s Expanded Edition lexicons (online, retrieved 13 May 2020)

[30] Hebrews 2:11-15, The Holy Bible Complete Jewish Bible translation (online, retrieved 13 May 2020)

[31] Natan Odenheimer, The Kabbalist Who Would Be King of a New Jewish Monarchy in Israel, Jewish Forward October 14, 2016 (online, retrieved 13 May 2020)

[32] Yitsḥaḳ Ginzburg, Avraham Arieh Trugman, Moshe Yaakov Wisnefsky, The Alef-beit: Jewish Thought Revealed Through the Hebrew Letters (Oxford: Rowman & Littlefield 1991)

[33] Yehuda Shurpin, Why No Vowels In The Torah?, chabad.org (online, retrieved 12 May 2020)

[37] Maria Carmela Betrò, Hieroglyphics: The Writings of Ancient Egypt (New York: Abbeville Press 1996), p.113, cit. the Egyptian Treatise on Ophiology – “The strange observation about the pain of the bite finds no comparison in modern medical texts.

[38] Jay Michaelson, Kabbalah and Queer Theology: Resources and Reservations, Theology & Sexuality, Vol. 18 No. 1, January, 2013, cit. Elliot Wolfson, Circle In The Square: Studies in the Use of Gender in Kabbalistic Symbolism (New York: State University 1995)

[39] Elliot Wolfson, Language, Eros, Being: Kabbalistic Hermeneutics and Poetic Imagination (New York: Fordham University Press 2005)

[40] Aryeh Kaplan, Sefer Yetzirah, The Book of Creation (Revised Edition), p. 32

[41] George Orwell, Nineteen Eighty-Four (2003 Plume Centennial Edition), p. 218

[42] Jay Michaelson, Op. Cit.

[43] Marcy Oster, Sephardi leader Yosef: Non-Jews exist to serve Jews, The Forward, 18 October 2010 (online, retrieved 13 May 2020)

[44] Moshe Idel, Kabbalah in Italy (1280-1510): A Survey (New Haven: Yale University Press 2011), p.198 –

Although a proclivity toward magic was conspicuous in an important circle of Spanish Kabbalists during the 1470s,it took a totally different direction. Unlike the magia naturalis , accepted by Ficino, Pico, Alemanno, and to a lesser degree David Messer Leon, the group of Kabbalists in Spain cultivated a violent, demonic form of magical Kabbalah intended to destroy the prevailing historical and religious order, including Christianity, for the sake of bringing the Messiah. It was a redemptive rather than a natural magic, focused upon solving historical rather than personal problems

Doublethink means the power of holding two contradictory beliefs in one’s mind simultaneously, and accepting both of them.

These contradictions are not accidental, nor do they result from ordinary hypocrisy: they are deliberate exercises in doublethink. For it is only by reconciling contradictions that power can be retained indefinitely. In no other way could the ancient cycle be broken. If human equality is to be forever averted—if the High, as we have called them, are to keep their places permanently—then the prevailing mental condition must be controlled insanity.

George Orwell, Nineteen Eighty-Four

Oh the irony.

Or perhaps rather, the karma.

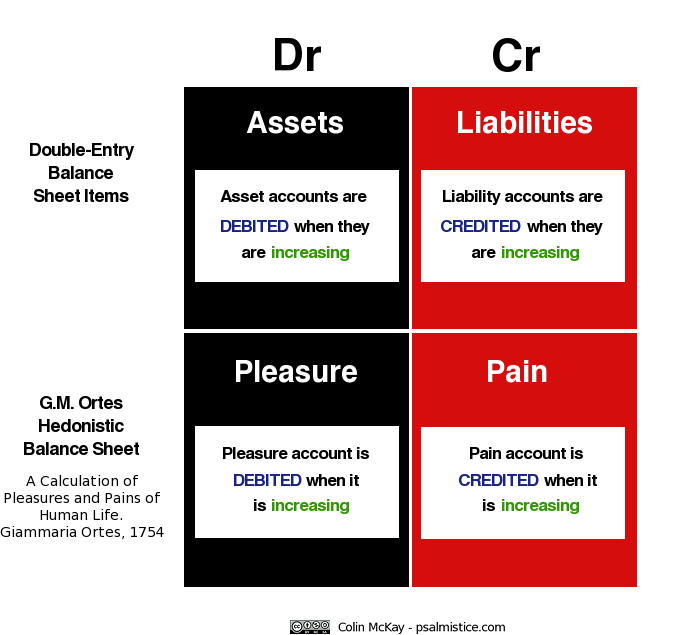

From the birthplace of el modo vinegia (“the Venetian Method”) of Double Entry Bookkeeping, and the modern banking Usurocracy that it spawned more than half a millennium ago, comes academic confirmation of the “outright false accounting” and “double nature” of bank ‘money’.

Professor of Accounting Massimo Costa, along with former international financial markets professor and current World Bank and IMF advisor Biagio Bossone, have confirmed that so-called “money of account” created by Double Entry Bookkeeping is a “systematically concealed” tool for extracting “seigniorage rent” from the labour of the human race.

In academic jargon, it is “a structural element of subtraction of net real resources from the economy, with potentially deflationary effects on profits and/or wages, distributional consequences, and frictions between capital and labor.”

In other words, the global banking system is an enormous parasite, and its parasitic method is fraudulent.

Their article relates to the heart of my essays (eg, here, here, here, here, here) on the ancient, alchemical philosophistry – the word ‘magic’ with numbers added – on which the ‘modern’ banking system is built.

More generally, absent adverse economic or market contingencies inducing depositors to convert deposits into cash, the liabilities represented by deposits only partly constitute debt liabilities of the issuing bank, which as such require [central bank] reserve coverage. The remaining part of the liabilities is a source of income for the issuing bank – income that derives from the bank’s power to create money. In accounting terms, to the extent that this income is undistributed, it is equivalent to equity.

This double nature of demand deposits is stochastic in as much as, at issuance, every deposit unit can be either debt (if, with a certain probability, the issuing bank receives requests for cash conversion or interbank settlement) or equity (with complementary probability).

Despite the fact that they claim to have loaned us all this money, thanks to the magical paradox at the heart of double-entry accounting, they also claim, simultaneously, precisely the opposite to be true — that we have actually loaned all that money to them.

[..]

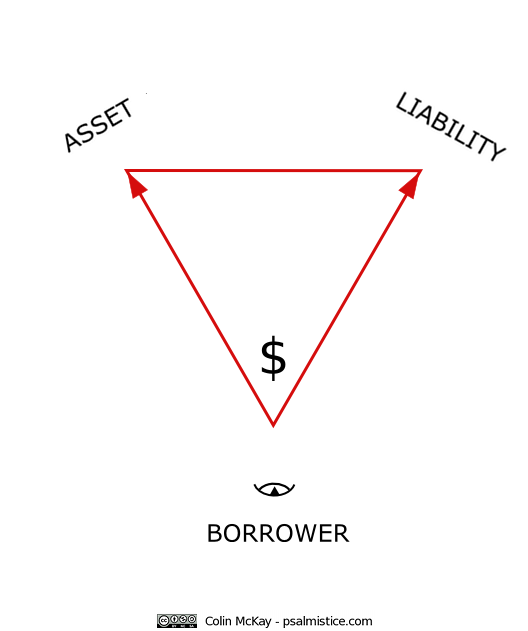

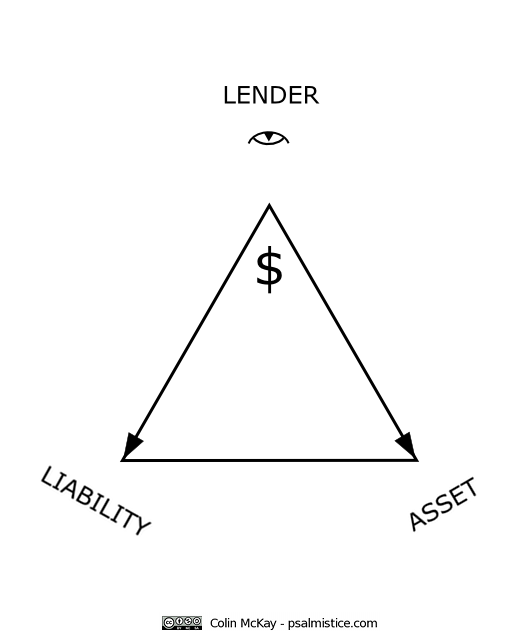

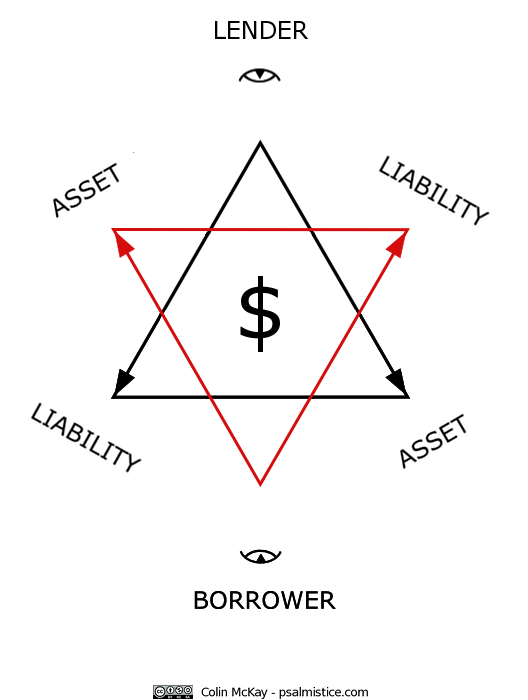

Believe it or not, there is an explanation—albeit a perverse, morally abhorrent and unconscionable explanation—for this, and in turn, for how the creeping global preparations to legally steal the “deposit” assets of bank customers (refer above diagram) is able to be “justified” by the banks, the financial and political authorities, and the unelected, BIS-funded, Goldman Sachs alumni-chaired FSB.

At the heart of the matter is the ever-present paradox of perspective inherent in the BabylonianDuality Principle on which double-entry accounting is based.

Banks are able to create new (so-called) ‘money’ ex nihilo through the loan origination process. As this is recorded using double-entry accounting, every new loan results in a new Asset and a new Liability on the banks’ balance sheet records.

However, because banks act both as new loan (thus, new ‘money’) originators and as financial intermediaries, there is no way of disaggregating the Liability side of any bank’s balance sheet in order to clearly distinguish between those “deposits” that have arisen in consequence of that bank’s own lending (so-called), and those “deposits” that have arisen in consequence of that bank’s intermediation (i.e., ‘transfers’ of ‘money’ from one customer account to another customer account at the same bank, or, from the customer accounts of other financial institutions to customers of the bank).

Whether or not any particular unit of any particular “deposit” amount could truthfully be defined as ‘money’ loaned to the bank by a customer, or, loaned by the bank to a customer, is dependent on knowing with complete certainty how and when each and every unit came to be recorded in the customer account. The only customer account for which such certainty is possible, is a customer account created by the bank at the moment of first originating a loan, and, before any new entry for even one single fractional unit of the denominated currency has been either added to, or subtracted from that customer account.

There is one further exception – an account established for one of the bankers’ favourite clients—arms dealers, drug cartels, mafioso, and other criminal organisations such as the CIA—at the first moment of the client handing over real legal tender cash notes at the bank to open the account.

In any event, since even a ‘transfer’ of ‘money’ from one bank to another still has the same ultimate origin—an out-of-nothing creation of an electronic record of a mutual exchange of promises to pay—then from a whole-of-banking-system perspective it really doesn’t matter; all so-called ‘money’ on ‘deposit’ is simultaneously owned by the customers, and by the banks.

In other words, the global Usurocracy’s rent-extracting ‘money’ system is based on the arbitrary, subjective, relativist ‘logic’ and philosophistry of Cabala, or what George Orwell called doublethink – “the power of holding two contradictory beliefs in one’s mind simultaneously, and accepting both of them.”

Doublethink is related to, but differs from, hypocrisy and neutrality. Also related is cognitive dissonance, in which contradictory beliefs cause conflict in one’s mind. Doublethink is notable due to a lack of cognitive dissonance—thus the person is completely unaware of any conflict or contradiction.

Thanks to 503 years of “progressive” regulatory capture – amounting to nothing less than a thinly-concealed regime of state-sponsored Usurocracy – it is the banks’ exclusive privilege to ‘earn’ compounding usury on all the self-annihilating, +1|-1 Double Entry ‘money’ units that they create out of nothing:

Owing to double nature of commercial bank money, a relevant share of the deposits that banks report in the balance sheet as ‘debt toward clients’ generates revenues that are very much similar to the seigniorage rent extracted by the state through the issuance of state money (coins, banknotes, and central bank reserves).

Costa and Bossone confirm that it is precisely this “double nature” of bank ‘money’ that enables banks to hide the reality of their extracting “seigniorage rent” from the labour of the human race. How?

By not recording the value of their imaginary accounting ‘money’ – supposedly “equivalent” to, or, in more honest words, a counterfeit of, real physical government legal tender cash notes and coins – on their Income Statement:

Under current accounting practices, seigniorage is largely underappreciated, it is systematically concealed, and is not allocated to the income statement (where it naturally belongs), while it is recorded on the balance sheet under debt liabilities, thus originating outright false accounting.

As I extensively evidenced, this fraudulent system is actively aided and abetted by the “secretive”, tax haven-registered, “private” corporations of the international accounting standard-setters; a fact also confirmed – tacitly – by Costa and Bossone:

The stochastic double nature of bank money is consistent with the principles of general accounting as defined in the Conceptual Framework of Financial Reporting, which sets out the concepts underpinning the International Financial Reporting Standards (IFRS). In light of these standards, demand deposits are a hybrid instrument – partly debt and partly revenue. The debt part relates to the share of deposits that will (likely) be converted into cash or reserves, while the revenue part relates to the share of deposits that will (likely) never be converted into cash or reserves. This share of deposits is a source of revenue.

The Mercurial Rebis: A Crowned and Bat-winged Hermaphrodite, Buch der heiligen Dreifaltigkeit, late 14th Century (Munich MS, Bayerische Staatsbibliothek, CGM. 598). Source: Adam McLean, alchemywebsite.com

What Costa and Bossone (conveniently?) neglect to mention is that the share of so-called ‘deposits’ that “will (likely) never be converted into cash or reserves”, and that is thus “a source of revenue,” is around 97%.

Rather like the banks conveniently neglecting to mention the same 97% on their Income Statement.

Apparently it is sufficient to describe what is in reality the vast majority as merely “a relevant share”.

In “Dishonourable Debt” we saw that effective July 1, 2009 – in the middle of the global banking liquidity crisis known as the “GFC” – the Financial Accounting Standards Board (FASB) introduced Accounting Standards Codification (ASC) §305 Cash andCash Equivalents. This new standard effectively sanctioned – and further concealed – the banks’ misleading and deceptive conduct in renting their electronic records of promises to pay physical cash under the guise of so-called ‘money’. As I observed:

The FASB has ex post facto codified that banks may consider bank ‘credits’ (a record of a promise to pay cash) as actually being “cash” for accounting purposes; that the customers’ perspective of bank ‘credits’ “shall” be that those ‘credits’ are (literal physical) “cash”, and, that they are not amounts owed to them by the bank…

Pure Orwellian doublethink.

This should help us to understand the real reason why, for several decades, there has been an accelerating drive by the international banking system to ‘normalise’ numerous forms of electronic banking and ‘money’ – including crypto currencies – and more recently, to actively discourage and even to incrementally (“Boiling Frog” strategy) restrict or outright ban the use of physical cash.

Contrary to all propaganda, this carrots-and-sticks drive towards a global economy reliant on pure abstraction, rather than real physical currency, has nothing to do with improving “convenience” for the public, or “efficiency” in the banking system, much less with “fighting crime” or “the black market”.

Real physical cash – State legal tender – is perhaps the weakest link in the Usurocracy’s “golden chain” of Double Entry ‘magic’ enslaving the human race.

Real physical cash is what the Usurocracy is counterfeiting, using +1|-1 Double Entry nullities, and then “systematically” concealing by not reporting their counterfeit ‘cash’ on their Income Statements.

Once physical cash is eliminated, the promises-to-pay ‘money’ system will be fully “unfettered” and “independent” from the real, tangible world. It will exist solely in the abstract, “imaginary”, ‘magic’ paradox-riddled, counterfeit world (pun intended) of Double Entry Bookkeeping controlled by the Usurocracy.

“The bookkeeper can be king if the public can be kept ignorant of the methodology of the bookkeeping.”

Do read and share this outstanding resource compiled by Urunu: The Cashless Society.

The magic chain of speech was typified among the ancients by chains of gold, which issued from the mouth of Hermes. Nothing equals the electricity of eloquence.

To make the Magic Chain is to establish a magnetic current which becomes stronger in proportion to the extent of the chain.

The Great Work in Practical Magic .. is the formation of the magnetic chain, and this secret is truly that of priesthood and of royalty. To form the magnetic chain is to originate a current of ideas which produces faith and draws a large number of wills in a given circle of active manifestation. A well-formed chain is like a whirlpool which sucks down and absorbs all.

– Éliphas Lévi, Dogme et Ritual de la Haute Magie, (1855)

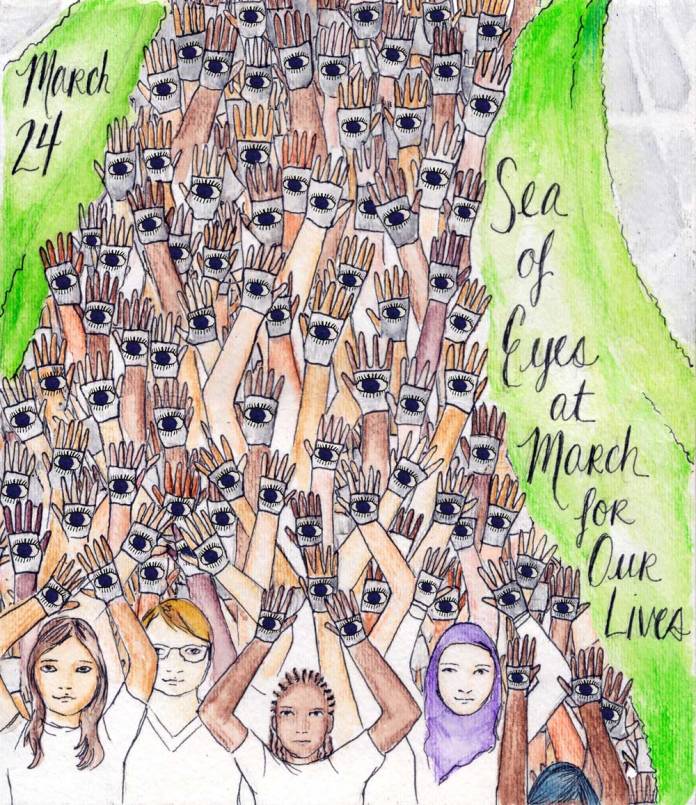

But whose lives, exactly, are the “our” lives that you marched for?

To find the answer, let us examine the hidden forces behind this well-organised, well-funded social movement, one that is purported to be “created by, inspired by, and led by students.”

Democratic strategists probably view the public uproar over the Las Vegas massacre and the continued persistence of school shootings as a gift from heaven or hell.

No, it is not simply the Democrats. Their involvement, and that of the liberal celebrity set, is hardly hidden – it is plain for all to see.

Depending on one’s philosophical leaning, these forces are either “miraculous” (Jewish), or “magical” (left-hand path, ‘Black Magic’).

The “miraculous” is associated with beliefs derived from the Babylonian Talmud, and commemorated since the Middle Ages as The Great Sabbath – a celebration of the mythical “War of the Egyptian Firstborn” against their own government.

Last Shabbat was Shabbat haGadol, the Great Shabbat, the last one before Pesach. It was also the occasion for another ritual, that national gathering called the March for Our Lives.

The “magical” is associated with Cabalist theurgical beliefs derived from ancient Babylonian astrology, numerology, alchemy, and the conjuration of “spirits” (angels and demons).

How well stated it was, how timely. This week, for the Sabbath before Passover, Shabbat HaGadol, the Great Sabbath .. Could the connection be any better?

As we will see, March For Our Lives also has much in common with the ‘Black Magic’ ritual methodology used by the Nazi Third Reich, “to focus attention on the cause and shape and nature of the cause.”

The importance of ritual and spectacle, public and private, is obvious to anyone who has seen films of Nazi rallies, parades, and so on. The National Socialists were modern masters of symbolism and ritual – what would be called Lesser (Black) Magic in left-hand path circles today. (Nowadays only rock concerts and sporting events remain as pathetic attempts at this kind of spectacle.)

As individuals can be transformed by rituals, whole cultures can also be metamorphicized through collective participation in such rituals. Even marginally effective ones, if repeated often and long enough, will have some result. But it may take only one good jolt from a highly potent rite to have a profound and lasting effect. The Nazis used both kinds.[1]

Please note that our purpose here is not to comment on the pros versus cons of the gun control debate – whether in the U.S.A., or elsewhere. Our exclusive focus is on examining the occult ‘magic’ ritual devices that have been employed to influence public opinion.

The conscious and intelligent manipulation of the organized habits and opinions of the masses is an important element in democratic society. Those who manipulate this unseen mechanism of society constitute an invisible government which is the true ruling power of our country.[2]

To whet the readers appetite for this necessarily lengthy exposition, here following are the subject areas covered. Clicking on each title links to its respective segment. It is recommended however, that they be read in order. A brief summary is included here, for the impatient or time-pressed reader interested only in the bare minimum, sans historic illustrations, photos and other evidences, and explanations. Please consider the words of George Orwell in Nineteen Eighty-Four as you continue:

Crimestop means the faculty of stopping short, as though by instinct, at the threshold of any dangerous thought. It includes the power of not grasping analogies, of failing to perceive logical errors, of misunderstanding the simplest of arguments if they are inimicable to Ingsoc, and of being bored or repelled by any train of thought which is capable of leading in a heretical direction. Crimestop, in short, means protective stupidity.[3]

Shabbat HaGadol – War of the Egyptian Firstborn Talmudic legend: Egyptian firstborn took up arms against their own government, hoping to compel Pharoah to grant freedom to the Hebrews, and thus save themselves from Moses’ 10th plague, the Angel of Death. Jews cannot lie on Sabbath; the firstborns’ intervention, driven by self-interest, saved them from need to lie. Seen as “miraculous” transformation of evil into good for the Jews.

The “Tactical” Sefirot – Hod (8) – Means to an End Claim of 800,000 Washington attendance, 800+ global rallies debunked. Significance of number 8 in Cabalist ‘magic’ and mysticism. Feet as “means to an end,” hidden motive exact opposite of one presented. Hod (8) = left foot, evil side, retribution. Alchemical symbolism: left foot forward. Left-hand Path, occult magic, Tarot divination in context of 8, the Four Eights, Tetragrammaton, mirror reversal, and March For Our Lives logo.

‘Magic’ – Time-ing is Everything Time-dependency: key to success in invocation and command of angelic/demonic powers in medieval Cabalist texts. Brief overview of Cabalist ‘magic’ influences on Renaissance through Enlightenment to post-modern humanist philosophy. Western Establishment culture “spawned from intersections of modernist rationalism and occultist magic and mysticism.”

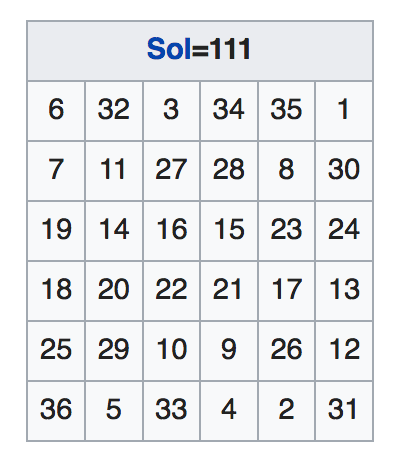

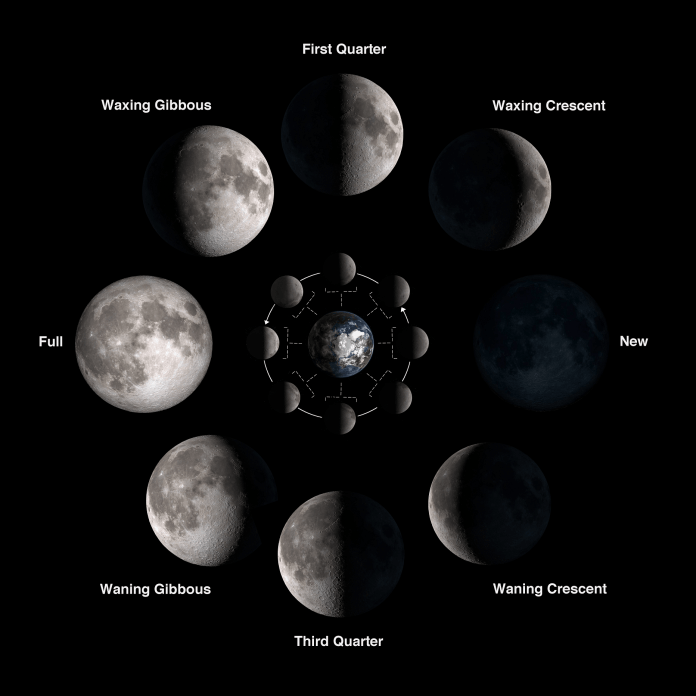

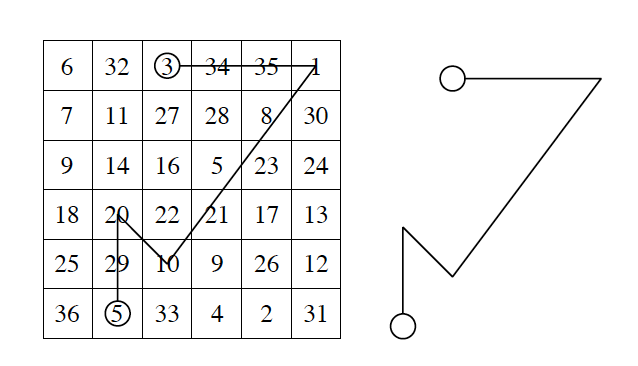

The Babylonian Sun Seal – Magic Square 111/666 Magical significance of David Hogg speech timing, and social media user names. Babylonian priests’ Magic Square, Sigillum Solis gold amulets. 111/666 connection. Washington rally stage symbolism, and the Rule of 72. The alchemists’ 🜓. “Dragon’s blood.” The Star of Raiphan / Chiun / Saturn / Satan and Shabbat (Sabbath) SaturDay. Lunar cycle: March 24 Half Moon, left side in darkness. Talmudic legend: Ashmedai / Asmodeus the “king of demons,” ruler of “good” Jewish demons, compelled through ‘magic’ to help build Solomon’s Temple, using his feet. Child sacrifice. Nachiel – the “intelligence of the sun”; angel controlling the sun: Hebrew letter gimel, “person in motion.” The Four Princes of the Evil of the World. Conjuration of the Four spirits of darkness.

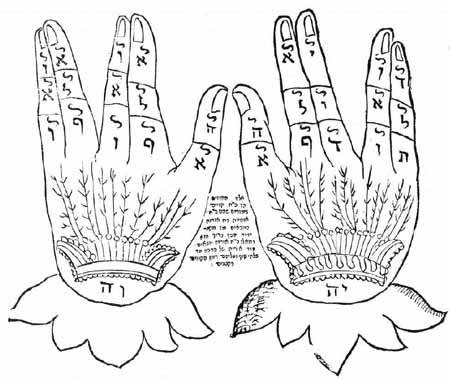

Hollywood Hamsa – Evil Eye amulet for Sabbath Pussyhat creator’s “Evil Eye Glove” promotion. History of Jewish hamsa (Evil Eye-in-palm of hand) talisman. The “Hand of Miriam” connection to timing of Great Sabbath celebration. Talmudic law allows carrying an “approved amulet” on the Sabbath, rabbinic exception to biblical prohibitions against magic, divination, and working on Shabbat.

Nazi ‘Black Magic’ – Weaponisation of Youth Ritual devices and methodologies. “Ceremonies of the Reich and the Course of the Year” liturgical calendar, replacement for orthodox Christianity. Springtime (late March) “commitment to the cause.” The Pledging of the Youth – David Hogg’s speech mirrors Hitler-Jugend / Bund deutscher Mädel rite of passage formula. Nazi “Holy Nights”, and leaving a chair for Elijah. The Chariot card. ‘Lesser’ Black Magic.

Hear the Chabad-Lubavitch organisation recount the tale:

The Talmud relates what happened when 600,000 Jewish heads of household began rounding up their lambs on the 10th of Nissan. The lamb was worshipped as a deity in ancient Egypt, so this caused quite a commotion. The firstborn of Egypt, who held the key social and religious positions in Egyptian society, confronted the Jews, and were told: “We are preparing an offering to G‑d. In four days, at the stroke of midnight, G‑d will pass through Egypt in order to execute the tenth and final plague; all firstborn will die, and the people of Israel nation will be freed.”

The firstborn, having already witnessed the first nine plagues occur exactly as Moses had warned, approached Pharaoh and his generals and demanded that the Jews be freed immediately. When Pharaoh refused, the firstborn took up arms against Pharaoh’s troops, killing many of them.

This “great miracle” is commemorated each year on the Shabbat before Passover, which is therefore called Shabbat HaGadol, “The Great Shabbat.”

Why do we commemorate the miracle on the Shabbat before Passover rather than on the tenth of Nissan, the date on which it actually took place? We see that the Torah itself mentions only the date rather than the day of the week.

It is because the miracle is closely connected to Shabbat. The Egyptians were aware that the Children of Israel observed Shabbat and did not busy themselves tending animals on that day, so when the Egyptians saw them taking lambs and binding them to their bedposts on Shabbat, they were surprised and decided to investigate what was happening.

The Children of Israel were in great danger when they were confronted and were saved only by virtue of a miracle. We therefore commemorate this miracle on Shabbat rather than on the tenth of the month of Nissan.

Moreover, had it not been Shabbat, the Children of Israel would not have needed a miracle to save them. They would have been able to deceive the Egyptians by diverting their attention or making up some kind of explanation. On Shabbat, however, they would not do so, for, as our Sages said, “Even an ignorant man will not tell lies on Shabbat.” Thus, we see that they were endangered because of their observance of Shabbat, and they needed a miracle to save them.

A further reason why we recall the miracle on Shabbat rather than on the tenth of the month is that, forty years later, Miriam [Moses’ sister] died on that day and the well which accompanied the Children of Israel and provided them with water in the wilderness, disappeared.[4]

The implication that it would be quite acceptable to lie and deceive – to break the 9th Commandment – on days other than the Sabbath, bears highlighting.

As does the first two tenets of satanic ideology: Self-Preservation, and Moral Relativism.[5]

For Hasidic and other esoterically-inclined Jews steeped in ‘magical’ interpretations of the Torah, the Babylonian Talmud, and cabalist texts such as the Sefer Yetzirah (ספר יצירה), Sefer Razi’el HaMalakh (ספר רזיאל המלאך) and the Zohar, this legend has long held another, “higher” significance. It symbolises the “miraculous” transformation of evil into good:

But is this simple victory of good over evil the final goal of Jewish teaching? Chassidic thought presents a higher ideal: transformation of evil into good, of darkness into light. On the national level, the enemy becomes a friend; on the inner personal level, the Evil Desire is transformed to good, and now works energetically in service of G‑d. [..]

This Shabbat before Passover, called the Great Shabbat (Shabbat HaGadol) also expresses the idea of transformation of bad to good.

The ancient Egyptians had enslaved and tortured the Jews. When Moses came with the Divine mission to bring the Jews to freedom, working one miracle after another, Pharaoh continued to resist. Yet on the Shabbat before the Exodus, commemorated by this Shabbat today, the Egyptian firstborn began to side with Moses, actively attacking their own government.

The Sages tell us that the attack was a response to the idea that the final plague, which had been forecast by Moses, would mean death for the firstborn. We might see it as no more than a reaction to personal fear. However, the Lubavitcher Rebbe points out that it was more than that. It was a transformation of the inner spiritual nature of existence. Ancient Egypt represented the depths of evil, implacably opposed to holiness, as indeed we see in the figure of Pharaoh himself. Yet on that Shabbat, what the Sages term a “great miracle” took place. Within Egypt itself, in fact the firstborn of Egypt – meaning the future leaders – began a movement on behalf of the Jewish people.

True, Pharaoh and the Egyptian authorities were not transformed at that point, and the tenth plague and then the Splitting of the Sea, destroying the Egyptian forces, had to follow. But the rebellion of the firstborn was a taste of the transformations of the future, when all darkness will be changed to light, and all violent evil to good.[6]

The “Tactical” Sefirot – Hod (8) – Means to an End

According to the website of March For Our Lives, Inc., the Washington DC rally was mirrored by “800+ sibling marches across the globe”. NBC and many others reported the event organisers’ claim that “800,000 people attended the march” and that, globally, “there were approximately 800 marches organized on Friday and Saturday — even one in Antarctica.”

This was sharply contradicted by CBS News, who reported the findings of Digital Design & Imaging Service Inc (DDIS), a Virginia-based firm which uses a proprietary method for calculating crowd size using aerial photos. According to DDIS, the peak crowd size was 202,796 people – one quarter (1/4) of the organisers’ claim – and the crowd reached its largest size at 1 pm.

Why tell such a bold lie? Is there perchance (or per design) a ‘magical’ significance to the number 8? If so, is that significance in some way relevant to this particular event?

Why yes. Let us count the ways.

In Cabalist doctrine, the eighth sephira (emanation) of “G-d” is the left “foot” of Adam Kadmon (Primordial Man), and is named “Hod” (הוד). Its opposite in the Cabalistic “Tree of Life” or “Gates of Light” is the seventh emanation (right “foot”), named “Netzach” (נצח).

The Jewish Encyclopedia (1906) informs us that “the conception underlying the cabalistic tree, of the right side being the source of light and purity, and the left the source of darkness and impurity” traces back “ultimately to old Chaldea.”[7]

Netzach and Hod: Means to an End Just like a loving parent may seem cruel when harshly disciplining a child in order to instill good values, the “tactical” sefirot of netzach [“victory”] and hod [“awe”] are often not what they seem.

When we call these sefirot “tactical,” we mean that their purpose is not inherent in themselves, but rather as a means for something else.

For example … I may use the tactic of kindness, though my intent may be antagonistic. I could lure an enemy into a trap by inviting him with a smile and a pleasant demeanor. The exterior façade of the act is pleasantness, its interior is punitive.

Netzach refers to actions of God that are chesed, “kindness,” in essence, but are presented through a prelude of harshness. Hod refers specifically to those events where the “wicked prosper.” It is retribution — gevurah, “strength/restraint,” in essence, but presented by a prelude of pleasantness.[8]

Gun control activism, presented with a pleasant façade, as a prelude to retribution?

Recall the praise of Jesus for the approaching Nathanael, who, on receiving news of him, had artlessly responded, “Can any good thing come out of Nazareth?” — “Here is an Israelite indeed, in whom there is no guile nor deceit nor duplicity!”

All the sefirot are likened to different parts of a body, and netzach and hod are likened to the two feet of a person: right foot and left foot.

Why feet?

Feet are usually only the means for a person’s activity. The hands are the main instrument of action and the feet are simply a vehicle to bring the person to the place in which he wishes to execute that action.

Secondly, the distinction between right and left foot is nowhere as pronounced as the distinction between the left and right hands. Similarly, while the distinction between chesed and gevurah is sharp, the distinction between netzach and hod is less sharp. Both are a mixture of chesed and gevurah and therefore the distinction is blurred.[8]

Revolution is “pleasant”, and pleasantness conceals retribution?

March For Our Lives, right left.

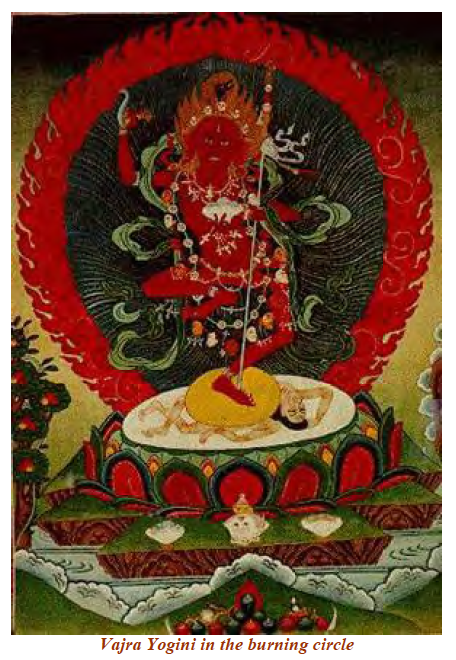

Readers of my previous essays on alchemy (“transformation”) may have noticed that in alchemical texts from both the East and West, the adept is typically illustrated in a left-foot-forward posture.

Vajra (“diamond scepter”) in the “Burning Circle”. (Source: Trimondi, The Shadow of the Dalai Lama: Sexuality, Magic and Politics in Tibetan Buddhism)

In occult traditions, the 8th sefira hod is described as “a force that breaks down energy into different, distinguishable forms, and it is associated with intellectuality, learning and ritual.” This is the ideology and method of the Left-hand Path: deifying the individual “Divine Mind.” Hod is said to be the sphere in which the magician mostly works. According to 19th century French occult magus Éliphas Lévi, hod represents “Eternity of the conquests achieved by mind over matter, active over passive, life over death.”[9]

In Hermetic-Qabalah, hod’s polar opposite in the Qlippoth (קְלִיפּוֹת), the Dark Side of the “holy sefirot” representing evil or impure spiritual forces, is a demon “called by the Hebrews, Samaël; by other easterns, Satan; and by the Latins, Lucifer”[10], the “angel of Mars”[11] (male, active, war); “The Desolation of God, or The Left Hand,” and its planetary symbol is Mercury ☿ .[12] In his book 777, the “Wickedest Man in the World” Aleister Crowley associated hod with the FourEights of occult tarot, and with Anubis, Thoth, Hanuman, Loki, Hermes, Mercury, Jackal, Hermaphrodite, Opal, Storax, and quicksilver.[13]

Éliphas Lévi affirmed this divinatory association (“The fourEights. Four times he triumphs on the timeless plane”[14]), emphasising that “The Key to the Great Mysteries will be established on the number four — which is .. also the number of the square and of force”:[15]

Turning now to the four suits, namely, Clubs, Cups, Swords, and Circles or Pantacles, commonly called Deniers all these are hieroglyphics of the tetragram [יהוה]. Thus, the Club is the Egyptian Phallus or Hebrew jod; the Cup is the cteïs or primitive he; the Sword is the conjunction of both, or the lingam, represented in Hebrew preceding the captivity by vau; while the Circle or Pantacle, image of the world, is the he final of the divine name.[16]

Observe carefully the four black silhouettes in the March For Our Lives logo, positioned exactly under the “UR” (meaning original, prototypical, primal; name of Abraham’s native city). Note the subtle difference in their forms: male-female-male-female (Left to Right), mirroring the jod-he-vav-heיהוה (male-female-male-female) in the (Right to Left) Hebrew script.

The eighth Major Arcana card in a traditional Tarot deck is Justice, and the eleventh card is Strength. Note the (“blurred,” “tactical”) correspondences to Jewish Cabala’s hod and netzach. Many modern Tarot decks, especially in the English-speaking world, have switched the numbering of these two cards to make them better fit the astrological correspondences derived by the English freemasonic Hermetic Order of the Golden Dawn. Éliphas Lévi tells us that the days of the moon possess a special character, corresponding to “the twenty-two Tarot keys.” The eighth day (Justice) is a “Day of expiation”, and signifies the “Murder of Abel” – the second-born (good) son of Adam and Eve – by Cain, the first-born (evil) son.[17]

Perhaps not coincidentally, in Jewish tradition the ‘magic’ covenant ritual of circumcision is performed on male children on the eighth day from birth.