In our ancient past, we traded between ourselves simply by drawing on our public reputation. We did favours for each other, and memorised — later, recording on clay tokens — the I Owe You. Our “currency” was our public Honour.

Today, bankers use the magick of double-entry bookkeeping to create IOUs out of nothing. These digital ‘tokens’ represent our IOU to the bank. Then — by a clever accounting trick — they let us ‘borrow’ their IOUs as ‘money’. Why don’t we all do the same thing, and just lend to ourselves?

Le bon Dieu est dans le détail (“the good God is in the detail”) means that attention paid to small things has big rewards.

MISLEADING PARLIAMENT

Imagine writing a paper for the Parliamentary Information and Research Service, correctly describing the Operational aspects of ‘money’ creation by the central Bank of Canada…

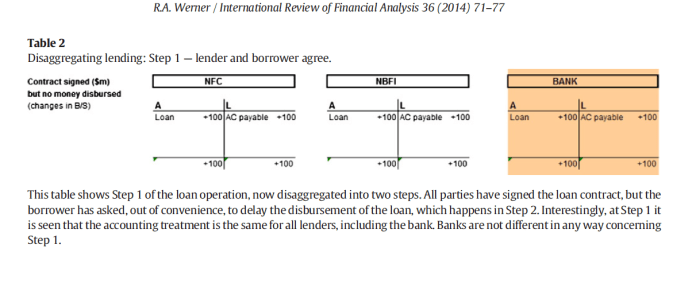

In practical terms, the Bank of Canada’s purchase of government securities at auction means that the Bank records the value of the securities as a new asset on its balance sheet, and it simultaneously records the proceeds of sale of the securities as a deposit in the Government of Canada’s account at the Bank – a liability on the Bank’s balance sheet (see Appendix A). No paper evidence of a bond, treasury bill or cash is exchanged between the Government of Canada and the Bank of Canada in these transactions. Rather, the transactions consist entirely of digital accounting entries. [..] By recording new and equal amounts on the asset and liability sides of its balance sheet, the Bank of Canada creates money through a few keystrokes.[3]

…but then showing the operation backwards:

Source: Library of Parliament, Canada

Step-by-Step: How It *Really* Works

Imagine describing and showing the identical (in law) process of ‘money’ creation by the Private Banking System, and getting that exactly backwards too:

Private commercial banks also create money – when they purchase newly issued government securities as primary dealers at auctions – by making digital accounting entries on their own balance sheets. The asset side is augmented to reflect the purchase of new securities, and the liability side is augmented to reflect a new deposit in the federal government’s account with the bank.

However, it is important to note that money is also created within the private banking system every time the banks extend a new loan, such as a home mortgage or a business loan. Whenever a bank makes a loan, it simultaneously creates a matching deposit in the borrower’s bank account, thereby creating new money (see Appendix B). Most of the money in the economy is, in fact, created within the private banking system.

A key similarity between money creation in the private banking system and money creation by the Bank of Canada is that both are realized through loansto the Government of Canada and, in the case of private banks, loans to the general public.

The legal reality is that banks do not lend money:

What they do when they make loans is to accept promissory notes in exchange for credits to the borrowers’ transaction accounts. Loans (assets) and deposits (liabilities) both rise by [the same amount].

It is important to notice here that the “Loans (assets)” are not loans to the borrowers. The “assets” of the bank are the promissory notes (promises to pay) issued by the borrowers.

Homeowners usually think of their mortgage as an obligation to repay the money they borrowed to buy their residence. But actually, it’s a promissory note they also sign, as part of the financing process, that represents that promise to pay back the loan, along with the repayment terms.

Banks ‘purchase’ promissory notes (“securities”) from the public, and from the Government. Then, they record – not their payment, but their promise to pay – as a ‘credit’ (i.e., a ‘deposit’) to a customer or Government account at the bank.

These ‘deposit’ accounts are recorded as a Liability on the bank’s Balance Sheet. This means that the bank has not paid. The bank still owes payment* to the customer. The so-called ‘deposit’ is fictitious.

(* Legal tender: cash notes and coins)

Stated another way, the bank ‘buys’ our IOU, and ‘pays’ for it with … its own IOU!

Incredibly, the bank then claims that its IOU to us (‘deposit’) is, simultaneously, our ‘credit’ (loan) to the bank.

As ‘depositors’, legally, we are “unsecured” creditors of the bank.[6]

In other words, the bank did not really give us ‘credit’; we gave our ‘credit’ to the bank … and that record is what we use as money.

We are paying the banks “interest” for the privilege of using our own money.

Why don’t we all just give our own ‘credit’ … to ourselves?

Read this, and think carefully on the clever words, “in effect”:

In today’s world of computerized financial transactions, the Federal Reserve Bank pays for the securities with an “electronic” check drawn on itself. [..] The Federal Reserve System has added .. securities to its assets, which it has paid for, in effect, by creating a liability on itself…

(Keep that concept in mind. Drawing. A liability. On yourself. I will be showing you a revolutionary new accounting system, where everyone can do this. We could become our own central bankers, and begin to solve many global problems, sustainably.)

Source: kateraworth.com

There is no need to take my word for this.

Or, indeed, the word of the Federal Reserve Banks.

I produced the first empirical studies[8] to prove that in the five thousand year history of banking.

The law courts in various judgements have made it very clear, if you give your money to a bank – even though it’s called a ‘deposit’ – this money is simply a loan to the bank.

They invent fictitious customer deposits.

The banks create the money supply by inventing these claimson themselves, the fictitious deposits.

The modern banking system manufactures “money” out of nothing; and the process is, perhaps, the most astounding piece of “sleight of hand” that was ever invented. [..] Banks in fact are able to create (and cancel) modern “deposit money”, just as much as they were originally able to create, or call in, their own original forms of private notes. They can, in fact, inflate and deflate, i.e., mint, and un-mint the modern “ledger-entry” currency.

He was the last of the magicians, the last of the Babylonians and Sumerians, the last great mind which looked out on the visible and intellectual world with the same eyes as those who began to build our intellectual inheritance rather less than 10,000 years ago.

Why do I call him a magician? Because he looked on the whole universe and all that is in it as a riddle, as a secret which could be read by applying pure thought to certain evidence, certain mystic clues which God had laid about the world to allow a sort of philosopher’s treasure hunt to the esoteric brotherhood. He believed that these clues were to be found partly in the evidence of the heavens and in the constitution of elements .. but also partly in certain papers and traditions handed down by the brethren in an unbroken chain back to the original cryptic revelation in Babylonia.

Early 13c., “of or pertaining to the head,” from Old French capital, from Latin capitalis “of the head,” hence “capital, chief, first,” from caput (genitive capitis) “head” (from PIE root *kaput- “head”).

We the general public, and the governments of the world, are dupes.

The human race has repeatedly been duped by the “sleight of hand” and quicksilver tongues of temple scribes, silver merchants, goldsmiths, and bankers, for thousands of years.

There was already a grave problem with merchants creating and issuing ‘receipts’ for fictitious ‘deposits’ almost 4000 years ago. The sixth king of the First Babylonian Dynasty tried to stop it:

If any one buy from the son or the slave of another man, without witnesses or a contract, silver or gold, a male or female slave, an ox or a sheep, an ass or anything, or if he take it in charge, he is considered a thief and shall be put to death.

Hammurabi Code of Laws, Number 7 (c. 1790 BC) [11]

Hammurabi Code of Laws, c. 1790 BC. (Louvre Museum)

By the time of King Nebuchadnezzar I (c. 1124-1103 BC), the ‘smiths had a new trick to avoid being caught in this *cough* capital crime. They discovered how to create fake silver, and use it to counterfeit the royal standard ingots.

Perhaps they even called it “Full Reserve” banking?

Their “royal art” is now known as alchemy; the art of transforming comparatively worthless, ‘base’ materials – like copper ♀, vinegar, oil, flour, milk and honey – into ‘pure’ and ‘precious’ counterfeits:

“Do not be careless (with respect to these instructions). Do not [show] (the procedure) to anyone!”

The text obviously describes a method of producing a silver-like alloy from base metal ingredients — the “leukosis* of copper” of alchemistic fame. The purpose of the operation is to deceive and the final formula [“this (kind of) silver cannot be detected”] is to allay any possible doubts of the “chemist”.[12]

* whitening

In 290 AD, Emperor Diocletian ordered the destruction of all manuscripts in the economic crisis-stricken empire on the topic of alchemy. Two manuscripts from Egypt written in Greek survived, and these papyri make it easy to understand why:

Several of the recipes speak quite explicitly about the economic purpose of these processes. Such phrases occur as e.g. “(alloy) imitating silver* of such a kind that it cannot be found out”, “this will be… of the first quality which will deceive even the artisans”, or “the metal will be equal to true… so much as to deceive even the artisans”.[13]

* Rome’s traditional metal currency (silver dēnārius)

By the early 14th century, the discovery of how to create highly corrosive acids had placed new weapons in the alchemists’ armoury. The need for secrecy was now being met through a complex array of cryptic allegories, symbols, euphemisms, and double, triple, or even greater multiple (Orwell’s doubleplus?) entendres:

Luna [☽ silver] is also yellowed similarly with a solution of Mars [♂ iron]. The method of that yellowing which is perfected by vitriol [🜖 sulphuric acid] or copperas [🜨 green vitriol] is as follows… Then it should be dissolved into a redwater to which there is no equal.[14]

At the dawning of the Age of Reason, a recipe of the famous alchemist Basil Valentine – likely pseudonym of Johann Thölde, owner of a salt-works in Thüringia – offers us a glimpse of the “hidden” influence of alchemy on ‘modern’ systems of thought … and banking practice:

..in the bottom of the glass you will find the treasure, and fundamentals of all the Philosophers, and yet known to few, which is a red Oil, as ponderous in weight, as ever any Lead, or Gold may be, as thick as blood, of a burnt fiery quality.[15]

Book of Abraham Lambspring – Nicolaum Maium 1607

The sleeping Father is here changed

Entirely into limpid water,

And by virtue of this water alone

The good work is accomplished.

(Note the “hidden hand” (left), and the right hand making the sign of the 21st Hebrew letter, שshin (šīn). It stands for Shaddai, a name for God. In the Sefer Yetzirah this “Mother Letter” means King over Fire: “He Made Shin King Over Fire, And He Tied A Crown To It” .. “the hissing ש corresponds to the hissing fire”.)

Today, we are enslaved by what two Italian professors recently called “outright false accounting”:

Under current accounting practices, seigniorage is largely underappreciated, it is systematically concealed, and is not allocated to the income statement (where it naturally belongs), while it is recorded on the balance sheet under debt liabilities, thus originating outright false accounting.

If money is accounted as debt, instead of correctly being considered as equity of the issuing entities and wealth for the society using it, it inevitably introduces a deflationary bias in the economy…[16]

This trick is not new.

It is simply the ‘modern’, electronic, government-licensed version of the same trick that ‘smiths and alchemists have used for millennia, to extract a special kind of “rent” from the sovereign, and the public.

1610s, “a person’s wealth,” from Medieval Latin capitale “stock, property,” noun use of neuter of Latin capitalis “capital, chief, first”.

[The term capital] made its first appearance in medieval Latin as an adjective capitalis (from caput, head) modifying the word pars, to designate the principal sum of a money loan. The principal part of a loan was contrasted with the “usury” – later called interest – the payment made to the lender in addition to the return of the sum lent.[17]

The difference between the value of money (its “purchasing power”), and the cost to produce it, is called seigniorage. The word comes from Old French, meaning “right of the lord (seigneur) to mint money.”

Minted coins bear an image of the bust or head (capital) of the sovereign – the “lord” of the land – because he/she is the creator (issuer) and owner of the coins. In accounting terms, the coins are the equity of the lord.

And they brought Him a dēnārius [a day’s wage]. And Jesus said to them, “Whose likeness and inscription is this?” They said, “[The Emperor Tiberius] Caesar’s.” Then He said to them, “Then pay to Caesar the things that are Caesar’s; and to God the things that are God’s.”

The lord ‘issues’ new currency into the community, by using it to purchase something of value from his/her subjects. No matter what substance it is made from – no matter what its real value, in any other context – the coin’s face (“nominal”: named) value, and the requirement to accept it in payment, is decreed by the authoritative Word of the “Lord” (“fiat”):

Legal tender is any official medium of payment recognized by law that can be used to extinguish a public or private debt, or meet a financial obligation. The national currency is legal tender in practically every country. [..] A check, or a credit swipe, is therefore not legal tender; it merely represents a means by which the holder of the check can eventually receive legal tender for the debt.[18]

Even though the citizens now hold the coin, and use it as currency between themselves, the “Lord” still owns it, and may demand its return at any time, (e.g.), in payment of a tax ‘obligation’ (debt).

In effect, at any moment in time, a citizen and the “Lord” both claim to own the coin. And we know what happens when someone tries to fight the will of the “Lord”.

If that seems rather unjust to you – even tyrannical – then you are not alone.

Nicole Oresme (1320-1382) was one of the first medieval theorists who did not accept the right of the monarch to have claims on all money. Standard excuses, such as a “budget emergency”, did not hold water (pun intended) with Oresme. He stated that any ruler who reclaims monies they have previously issued (spent) is a “Tyrant dominating slaves.”[19]

In the Middle Ages, when commodity (metallic) money was standard, seigniorage was a tax added on to the cost of producing coins by the mints. A customer (e.g., a prince or feudal lord) who wished to issue coinage for trade within their own feudom or “fief” paid this tax, often in the form of a percentage of the metal delivered to the mint for coining, which was then passed on to the sovereign (king, queen) of the land.

Today, the ‘sovereign’ government ‘earns’ seigniorage profits in a similarly circuitous manner. Its profits are routed – pun intended – via the “independent” Central Bank:

In Canada today, seigniorage can be calculated as the difference between the interest the Bank of Canada earns on a portfolio of Government of Canada securities—in which it invests the total value of all bank notes in circulation—and the cost of issuing, distributing, and replacing those notes.

After deducting the Bank’s general operating expenses .. the remainder is paid to the Receiver General for Canada.[20]

In the case of the U.S. Federal Reserve System, its twelve Member banks are owned by private banks. The Fed pays a ‘return’ (dividend) of up to 6%[21] to those banks, before returning its leftover profits to the U.S. Treasury:

[T]he Reserve Banks are required by law to transfer net earnings to the U.S. Treasury, after providing for all necessary expenses of the Reserve Banks, legally required dividend payments, and maintaining a limited balance in a surplus fund.[22]

The Private Banking System also ‘earns’ a form of seigniorage profit or rent, called “monetary seigniorage”. It earns this on 97% of the ‘money’ supply. It is the difference between what it costs to produce their fictitious ‘deposits’ (i.e, nothing), and the interest and fees that we pay them for the use of what is actually our own money:

Commercial bank seigniorage represents structural element of subtraction of net real resources from the economy, with potentially deflationary effects on profits and/or wages, distributional consequences, and frictions between capital and labor.. .[23]

Perhaps it is now becoming evident why bankers see themselves as “doing god’s work”. They have succeeded in becoming gods of the earth. It is they who now create and issue the ‘currency’ we all use. They can and do demand its “return” – pun intended – as and when it suits them; typically, in a “liquidity crisis”. Having long ago usurped the powers of sovereigns, replacing them with an illusory rule of the dēmos (people), it is they who now ‘earn’ the vast majority of seigniorage profits from ‘money’ creation.

Thanks to the sleight of hand and mouth of the alchemists – hidden (“occult”) knowledge, that has been passed down for millennia in sexual allegories and symbols – the global money system is a cunning inversion (or reversal) of sovereign ownership rights.

We the People are, individually, the true seigneurs.

We – not bankers – are the true creators, issuers, and owners of the purchasing power (re-presented by “money”) used in the economy.

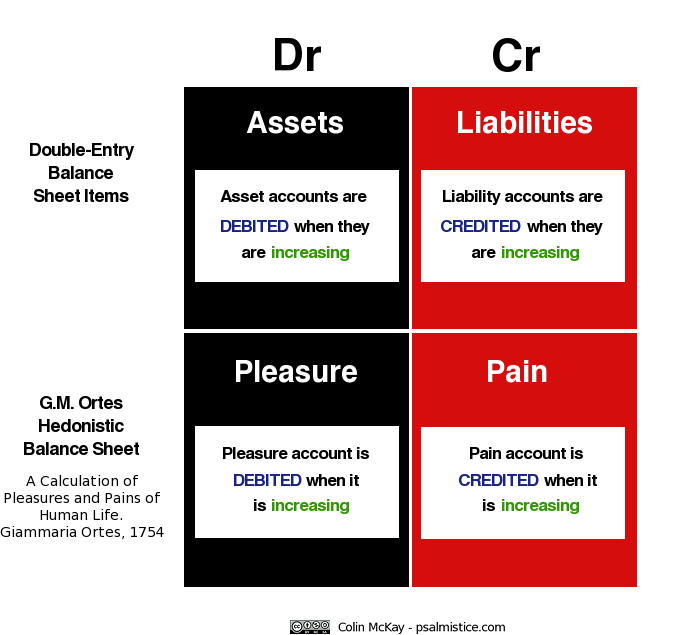

Through word ‘magic’ – especially puns; double entendres – and the paradoxical doublethink embedded in Double Entry Bookkeeping, bankers transform our wealth (equity) into debt.

Through this trick, they are able to ‘earn’ (steal) vast wealth and power for themselves.

Bankers have transformed themselves into the new Lords of Time. Their business is buying and selling our life times.

The business of banking can be – and indeed, has long been – defined as a ‘satanic’ practice. According to one of the founders of humanistic psychology, David Bakan:

A major psychological feature of black magic is that it provides immediate gains without immediate payment. The payment is feared as “really” both deferred and excessive. Thus deferred and excessive payment for immediate gain is characteristically associated with pacts with the Devil. The aversion towards usury, in current times as well as throughout the history of Christianity, is not completely coincidental. For usury is exactly a social expression of the Satanic Pact, immediate gains and excessive deferred payment.[24]

We ‘sell’ (promise) our future life energies to the bank, in exchange for a fictitious, lump sum ‘deposit’, or high usury ‘credit line’, now.

The bank ‘earns’ a covenantedflow of income from our labour, provided that we remain willing and able to pay, and, so long as the ‘sovereign’ remains willing and able to enforce the bank’s right to seize our real world assets pledged as collateral.

Over the long term, banks slowly acquire legal ownership title to all of our value-able assets, using their fictitious ‘loans’. The price of value-able assets is first driven up, thanks to the immediate availability of abundant, lump sum purchasing power, created by banks with a few keystrokes. Then, their price falls again, when the flow of new purchasing power ‘dries up’. Those who bought at the higher prices, are trapped paying usury on the ‘loan’ taken at the higher price. They have just been “fleeced”. Not just of ‘money’. They have been fleeced of the most precious ‘commodity’ of all .. life time.

Like the ‘loans’ themselves, the so-called “business cycle” is consciously, willfully, artificially created, by bankers, for the benefit of bankers.

–––––––– SIDEBAR ––––––––

Das guldene Vleiss (“The Golden Fleece”) Alchimiæ encomium. Vera chymia licet mundo sapientia falsa,

attamen est divæ diva parens sophiæ.

This 1737 alchemical text purports to show an image, dated to 1607, of ‘Sophia’ (Greek: σοφία), symbol of Wisdom in Hellenistic, Gnostic and Platonic philosophy and religion. In Orthodox and Roman Catholic Christianity, Holy Wisdom (Hagia Sophia) is an expression for God the Mother in the Trinity (Θεοτόκος, Theotokos), and often for the Holy Spirit, or Divine Logos, as personification of Christ.

What is depicted, however, is the alchemists’ androgyne god Hermes, or Mercury ☿ , as evidenced by his traditional symbol, the winged helmet. About his head, a nimbus of ‘light’. Around his neck, a pendant in the shape of a ‘heart’, womb, or ‘Water’ 🜄. The wealth in his left (Asset) hand, is the symbol of Venus ♀ (Female, Love, Beauty, Nature, Nurture), inverted, and bound; around the cross is a crown of thorns. On the left (Asset) wrist, a chain, from which a lamb is hanging. At his left foot, a pot of money, and treasure chest. Chained to his right (Liability) ankle, a ball with Mercury’s (“equal and opposite”) ‘wings’, adjacent alchemist’s flasks. ‘His’ robe exposes a female breast. There are twelve decorations on the hem; it is prominently secured at the top of ‘his’ thigh with one more decoration, a 4-petalled ‘flower‘ (🝊 wax, created by ‘drones’, labouring for a ‘Queen’, from whence golden ‘honey’; also 🜨 green vitriol), for a total of thirteen (number of lunar-menstrual cycles per year). In his right hand, a book opened, with an ‘eye’ on the left and right pages, and a serpent coiled around his arm.

The inverted and bound Venus, or orb and cross 🜭 , is the globus cruciger (Latin: “cross-bearing orb”), used from the early 5th century to represent Christ’s dominion over the world. In alchemy however, it is a symbol for cinnabar, or Mercury Sulphide. This is the source of two out of the three primary elements in alchemical ‘experiments’, and philosophy: the double-natured liquid-metal, Mercury ☿ (the “Divine Fiery Water” of Kabbalah), and Sulphur 🜍. The third element, is ‘Salt’ 🜔. Of the Earth 🜃. “The Body”. The ‘Base’ Matter. That must be subjected to Putrefaction 🝤. Reduced to a massa confusa (“confused mass”). Ringing bells? Look closely, at all the symbols. What do you see? Cinnabar 🜭 is also represented by 🜓 , a symbol of great significance (e.g., associated with Jesus’ life span; number of years between natural alignments of the pure lunar calendar and pure solar calendar.)

–––––––– END SIDEBAR ––––––––

There are other grave problems caused by bankers’ quest for profit. Making excessive new purchasing power available for consumption, and that of an increasingly vast array of products manufactured with a profit-driven goal of ‘Planned Obsolescence’ – i.e., poor quality – has dramatically accelerated humanity’s consumption of natural (and often, finite) resources.

This accelerated rate of production and consumption has, in turn, accelerated the production of waste, and pollution of the natural environment. While Mother Nature has her ways of recovering and restoring herself, it can take tens, hundreds, or hundreds of thousands of years for her self-healing processes – driven by her grateful receiving of energy from the Sun – to return Nature to anything like her former condition.

Allowing bankers to usurp our rights, as the seigneurs of our own money, and lords of the expenditure of our life’s time and energy, has not turned out well for many of us.

Even if we accept the narrow argument that capital-ism has “lifted millions out of poverty”, the manner and speed at which this has been achieved has not turned out well for our collective home – Mother Nature.

USURY

Sometimes, lest worse befall and to avoid scandal, a community tolerates dishonorable and evil things, like brothels. Sometimes also, by necessity or convenience, vile business is tolerated, like money-changing, or evil business, like usury.

Perhaps it is not an accident that the race which did most to bring the promise of immortality into the heart and essence of our religions has also done most for the principle of compound interest and particularly loves this most purposive of human institutions.

I see us free, therefore, to return to some of the most sure and certain principles of religion and traditional virtue – that avarice is a vice, that the exaction of usury is a misdemeanour, and the love of money is detestable, that those walk most truly in the paths of virtue and sane wisdom who take least thought for the morrow. We shall once more value ends above means and prefer the good to the useful. We shall honour those who can teach us how to pluck the hour and the day virtuously and well, the delightful people who are capable of taking direct enjoyment in things, the lilies of the field who toil not, neither do they spin.

But beware! The time for all this is not yet. For at least another hundred years we must pretend to ourselves and to every one that fair is foul and foul is fair; for foul is useful and fair is not. Avarice and usury and precaution must be our gods for a little longer still.

With the bankers’ system, our money becomes our debt, because we don’t spend it into existence; we ‘sell’ it to the bank, in return for a fictitious ‘loan’ from the bank, created out of nothing by the Word of the “lord”.

Instead of equity (wealth, purchasing power), our money is magically transformed into the exact opposite: our promise to re-pay the bank in the amount of their fictitious ‘loan’ … plus “interest” (usury).

On the other hand, the bank ‘deposit’ record created in our name is considered our loan to the bank, and the bank might pay us “interest” on it.

Unsurprisingly, the banks ‘earn’ a higher rate of usury on their Asset (our promise to pay them), than they pay on their Liability (their promise to pay us).

The difference in these rates is called the “Net Interest Margin” (NIM). It is key to how banks ‘earn’ so much ‘money’ in profit. It is the 24/7/365 reward for their hard labour, in taking our money, and then renting the use of their fictitious accounting ‘money’ back to us.

Book of Abraham Lambspring (1556)

I am told that the Danish, French, Germans and Italians do not use the words “Asset” and “Liability” as titles for Balance Sheet records. It would seem more than mere coincidence that they use their words for “Actives” and “Passives” instead.

How so?

In alchemy, the Active force is associated with the Male (Mars ♂, Fire), and the Passive with the Female (Venus ♀, Water).

copperas (n.)

A green,crystallineheptahydratemineral of ferrous [iron]sulfate,FeSO4·7H2O. Alsocalledgreenvitriol.

[MiddleEnglishcoperose, a metallicsulfate, fromOldFrench,fromMedievalLatincuperōsa, probablyshortforaquacuprōsa, copperwater, fromLateLatincuprum, copper]

Frenchcouperosé (adj., “blotchy”), from Latin cupri rosa, “rose of copper.”

Latin aes (“copper”) .. from the Latin form of the name of the island of Cyprus, where copper was mined (the alchemists associated copper with Venus).

Aes passed into Germanic .. and became English ore. In Latin, aes was the common word for “cash, coin, debt, wages” in many figurative expressions.

In the ‘modern’ money system, the Active (‘Male’) party is the bank. ‘He’ extracts usury from the Passive (‘Female’) party – the misled and deceived ‘borrower’.

Observe that even the usury that is ‘paid’ by the bank on its fictitious ‘deposits’, is recorded as if it were coming from the Passive (Liability, ‘Female’) side of its Balance Sheet.

Step-by-Step: How Banks Extract “Interest”

The fact is that from the earliest recorded times until the later Middle Ages even interest was forbidden by both canon and civil law, for interest then was synonymous with usury.

But the general detestation was diminished by 37 Hen. 8, c. 9 (1545) which, while entitled “A Bill Against Usury”, tacitly legalized it to a maximum of 10 per cent per annum. This statute inaugurated the serviceable fiction that usury no longer meant any interest, but only excessive interest.

The etymology of usury is from the Latin words usa and aera, meaning “the use of money”.

J.L. Bernstein, American Bar Association journal (1965) [27]

“Interest” (usury) is often called the “price” or “cost” of money. This cost is not just the price we pay for “the use of” the banks’ fictitious ‘deposits’. It is also a hidden cost, that is embedded in the prices of everything we buy.

Even those who imagine they have no debt, do, and are paying the price of someone else’s debt every time they go to a shop.

Indeed, even a ticket for “public” transport carries this hidden cost in its price.

Under this system, the bottom 80% of the population pay twice as much interest as they ‘earn’. The top 10% ‘earn’ twice as much interest as they pay. And the top 0.01% ‘earn’ 2000times more interest than the top 10% receive, on average.

The interestusury system is the Number 1 driver of inequality.

Little has changed, in 5000 years.

Professor Michael Hudson (How Interest Rates Were Set, 2500 BC – 1000 AD) informs us that usury “became the major force polarizing ancient society as credit passed out of the hands of public institutions into those of private households”:

The irony is the fact that the Latin term for loan interest was fænus. Its prefix (fe‑) connoted the idea of fecundity, much as the Greek word for interest/usury, tokos [“birth”]. Aristotle noted that unlike cows which reproduce themselves, metallic money lent out by usurers is sterile. This barrenness of metal is the central problem of usury: Interest is demanded on the basis of money-loans whose proceeds are not invested productively, much less at sufficient profit to pay the rates demanded by usurers. [..]

Creditors often broke up families by taking away their servant girls, daughters, sons or mother as debt pledges, while they themselves refrained from marrying in order to keep their own family fortunes intact. [..]

By classical Greek and Roman times, no palace rulers were left to cancel agrarian debts and otherwise keep creditor power in check. Thus, what seems to have begun as justifiable debt in third‑millennium Mesopotamia evolved into classical usury. Its corrosive dynamics polarized ancient society more than any other factor, destroying the archaic social balance between rich and poor, mercantile creditors and cultivators, despite the nominal decline in interest rates.

The power of creditors increased in the face of declining royal authority. Although the normal lending rate declined from Bronze Age Mesopotamia through classical Greece and Rome, creditors were able to render irreversible the forfeiture of land and personal freedom which debtors traditionally had been obliged to pledge as a condition for obtaining loans. In sum, what is first documented in Sumer is a revolutionary institution, revolutionary in that interest-bearing debt ended up by inciting populations to revolution at the end of antiquity, in the second and first centuries BC throughout the Romanized Mediterranean world.[28]

–––––––– SIDEBAR ––––––––

This slideshow requires JavaScript.

The discovery of strong mineral acids, particularly of HNO3, and aqua regia, had a strong effect on existing ideas about minerals, metals, and their chemical composition. For example, the discovery of aqua regia [“royal water”, 🜆] derived from vitriol* and sal ammoniac [🜹] robbed gold of its status as an indestructible metal, for now it could be dissolved, or “killed” as some alchemists would say. .. Indeed, green vitriol was often referred to as “the green lion” [“devouring the Sun”] in alchemical terminology, and the corrosive elixirs extracted therefrom caused it to be the subject of much secrecy, allegory, and interesting imagery in fourteenth century alchemical texts.[29]

* green vitriol 🜨 (iron ♂ sulphate), and blue or “Roman” vitriol (copper ♀ sulphate)

–––––––– END SIDEBAR ––––––––

‘People’s revolutions’ rarely occurred under the monarchies of ancient Mesopotamia. Their kings gained favour with the commoners by regularly using their royal authority to declare the people’s debts forgiven. All private debts were cancelled, family members sold (bankrupted) into slavery were free to return home, and any property forfeited was returned to the original owner.

This practice involved smashing the clay tablets on which the details of debt were recorded. Typically this occurred at New Year, and so the people were able to start over with “a clean slate.”

In the series Mr Robot, the hacker hero Eliot wishes to destroy the digital records of student debt held by EvilCorp. In accounting terms he is attacking the asset side of a bank’s balance sheet – destroying the digital records of what people owe the bank – but the same process could be applied to the data records of bank liabilities, the promises they issue to people, the ‘money’ we see in our bank accounts.[30]

In Sumerian, it was called ama-gi; in Akkadian, andurārum; and in Babylonian, mi’arum. The word meant the return of persons or property to their origin, or former status.

Readers of my earlier essays on the radically misogynous, predatory sex ‘magick’ principles in alchemy and banking may recognise a profound significance, and connection, in learning that the Sumerian word ama-gi derives from a noun ama “mother”, and the present participle gi “return, restore, put back”. Its literal meaning is “return to the mother”.

The same word in Hebrew (דְּרוֹר֙) meant “release”, “a flowing”, and “liberty”.

From an unused root (meaning to move rapidly); freedom; hence, spontaneity of outflow, and so clear – liberty, pure.

It is the word Jesus is reported as using in his first public sermon, when he stood in the synagogue and read from the scroll of Isaiah:

The Spirit of the Lord is upon Me, Because He has anointed Me to preach the good news to the poor. He has sent Me to announce release (pardon, forgiveness) to the captives, And recovery of sight to the blind, To set free those who are oppressed, to proclaim the favorable year of the Lord.

That word was deror.

DEROR

To radically shift regime behavior we must think clearly and boldly for if we have learned anything, it is that regimes do not want to be changed. We must think beyond those who have gone before us and discover technological changes that embolden us with ways to act in which our forebears could not.

If you think fundamentally, a banking licence is not given to everyone. It is only given to a certain organisation which fulfills certain criteria. So it’s a privileged licence.

Imagine a world where you could do exactly what banks do.

Pay with “an electronic check drawn on (your)self.”

Imagine if everyone could do the same thing – “create a liability” on themselves, and use it to buy goods and services from each other.

A world with no banks, and no usury.

The accounting is really quite simple. We need only to cut the banks out of the picture we have just been looking at, and internalise the same operations.

Imagine a world with no banks.

Unlike the banks, however, who “systematically conceal” the seigniorage value of the ‘deposits’ that they create out of nothing, cleverly taking that value for themselves (“seigniorage rent”), we will clearly show it, for everyone to see.

This can be done with an inverse public Honour rating, linked to both sides of your Balance Sheet.

In this accounting system, Single Entry is combined with Double Entry (SEDE). This means that most often, your “Balance Sheet” will not be balanced*. The amount on each side will be different. The side that is the largest determines your public Honour rating.

(* For readers keen on economic theory, this can be called a dynamic disequilibrium system.)

Let us see how it works.

Every time you draw a liability on yourself – that is, every time you create new purchasing power for yourself – your public Honour rating falls:

In this step, you have not actually used your new purchasing power (‘money’) to pay for something yet. You have simply created a matching Asset and Liability. Exactly like all the banks do. And your public Honour rating fell, according to the amount you created. Anyone you trade with can now see that you have “drawn” a liability on yourself, of 5%. The seigniorage value of the new purchasing power that you just created for yourself, has been publicly recorded.

(So, if you didn’t actually need to buy something right now, perhaps you should have waited, until you do? That way, the seller would see your perfect public Honour rating, at the Point-Of-Sale.)

When you do buy something, however, only the Asset side of your Balance Sheet is effected. Part of your new Asset is transferred to someone else. But your public Honour rating remains unchanged:

You created a debt (Liability), remember? In a real sense, that debt is not just a debt to yourself. Your creation of new purchasing power, out of nothing, bought you something (a benefit) that ultimately came from the natural world; consuming resources*, and/or human energy (life time). You need to give back – do something for someone else – to restore your public Honour.

(* Also, all human activities result in waste – pollution – in one or many forms. These real costs to the environment and society are “externalised” by current accounting methods. Some people profit – corporate ‘persons’. Everyone else suffers the costs.)

By selling something, or doing work for someone, you earn back purchasing power from others. Your debt (Liability) is reduced, and your public Honour rating rises.

In the following example, having spent3000 (above), you are now receiving a payment of 2000, which cancels some of your Liability:

As you can see, when you received purchasing power (i.e., a payment) from someone else, only the Liability side was effected.

That is because any payments received are first used to reduce any outstanding Liability amount that you have previously created, by drawing on yourself.

If you have no Liability – a zero (0) on the right side – only then will new payments received be added to your Asset side.

In other words, you must pay down your Liabilities; you cannot just accrue more Assets. In time, your worsening public Honour will incline others to refuse to deal with you.

Remember: your public Honour rating is determined by the largest side of your Balance Sheet. This means that simply building up more accounting Assets also harms your Honour rating. If you have them, it is wiser to spend them, which benefits someone else, as well as yourself. After all, you can always create more, when and if you really need it. In this way you can maximise your public Honour.

If you wish, you can transfer amounts internally – from your Asset side to your Liability side – in order to more quickly restore your public Honour rating.

For example, perhaps you have created more purchasing power than you actually need to spend right now. You can simply transfer your Asset, to cancel out some (or all) of your Liability:

This system is built on a set of rules that provide everyone with strong incentives to do the right thing. For themselves. For others. And for nature.

To use your seigniorage rights – that is, your individual sovereign right to create purchasing power – wisely, and sustainably.

By exercising self-discipline with your life’s time – by balancing your spending flow and your earning flow – you maximise your public Honour.

Alchemical symbol for Time (1 hour)

🝮

Alchemical symbol for Time (24 hours)

🝰

I-Ching, Hexagram 24 復 (fù): “Return”, The Turning Point, Renewal, Restore

Now, we all know that life can seem cruel at times. We make mistakes. And pay a price. Sooner, or later. Sometimes they are really big ones. And sometimes, despite our best efforts, things just happen to us.

We have accidents. We fall ill. Or someone we love does. The economy has a “downturn”. We lose our job. Our business fails. On it goes.

Many have tried to sell us the idea that “everyone is (born) equal” but let us be honest here, ok?

That is a plain, bald-faced lie.

For many, the ‘negative’ outcomes – at least compared to many others – begin before conception.

For some, extraordinarily ‘positive’ outcomes begin before conception.

I am confident, for example, that there are some who will read this essay – and many more who won’t – who are natural-born, genius intellects. Or at least, an awful lot smarter than I. And there are others, who are naturally gifted with an overabundance in particular drives, or aptitudes, and so will always be able to out-compete me, and you, in one way or another … and possibly in everything!

And that’s just fine by me. Personally, I cannot, and do not wish to imagine the bleak, colourless horror of a world without difference.

Frankly, I do not believe that mere imperfect humans are capable of conceiving a “perfect” system of exchange, that can ‘magically’ create a utopian outcome in a world of vast differences, and imperfections. To imagine that we can, I think, implies a degree of egotism that should encourage our caution.

I do believe, however, that after 5000 years of repeating exactly the same, fundamental mistakes when it comes to the design, and regulation of our mediums of exchange, that now we can design systems that are, at least, a lot more fair.

And, a lot more merciful.

This accounting system offers everybody exactly the same power to create purchasing power … coupled with exactly the same responsibilities.

So, it is only fair that it offers everybody the same amount of mercy.

And it gives this mercy – or grace – every week. Not once a year, or every seven, or forty-nine, or when a new king ascends the throne and wants to buy public favour.

Every seventh day, the algorithm cancels a percentage of the units from both sides of your Balance Sheet.

It restores your public Honour.

You might call it a small weekly Jubilee. Or andurārum, or mi’arum, or a return to the mother.

Or … grace. A little bit of forgiveness.

I call it Polarised Demurrage (“P.D.”).

It is a kind of “inverse” demurrage function, that operates the same way on both of the unequal and opposite “poles” of your Balance Sheet.

The following example illustrates how it works. To make it simpler (for me, to make the animation!), this only shows what P.D. will do with no new transactions by you, of any kind, over eight weeks.

Notice how both sides of your Balance Sheet reduce, and your public Honour rating climbs a little each week. It starts with you in the somewhat precarious position of only 60% Honour – because you are 40,000 in the red.

Any time you receive a payment, or, spend some of your Assets, or, create some more purchasing power for yourself, the algorithm will simply recalculate, and start the weekly forgiveness cycle over again.

The seventh day – the day that you receive some forgiveness – is determined by the date of the transaction that has taken you the greatest distance away from zero .. on either side of your Balance Sheet. Your personal “forgiveness day” will only change, if you exceed that number again, on a different day of the week.

Here is one more example, to illustrate how a new drawing of liability on yourself interrupts, and restarts, your forgiveness cycle. Again, you are starting 40,000 in the red, at 60% Honour.

After four (4) weeks worth of “forgiveness”, during which time you have (again) not made any new transactions of any kind, you decide to draw some more liability on yourself – another 3000.

The forgiveness cycle is shown continuing on for a further six (6) weeks, after your new “drawing” of 3000.

I hope that this has helped to show you that it is possible for us to eliminate the role of banks, and usury.

That it is possible to create a new system of ‘money’ and exchange, that returns our seigneur right to ourselves, and works fairly and equally for everyone.

An inversion, of their inversions.

It is not even a ‘money’ system, really. It is just a system for counting how much net benefit each one of us has gained, from the equal right to make withdrawals from other people’s – and nature’s – finite resources.

I think that a counting system like this would eliminate many problems caused by the greed of the ‘smiths and alchemists, and, provide benefits similar to those that many are now calling for – e.g., UBI, “living wage” – without having to beg banker-owned ‘sovereign’ governments for it.

Or trust that they will not abuse the increased power such regimes would give them, over our life times.

Or trust that we will not fall into ever more destructive habits of mind and action, as a result of increased dependency, without increased responsibility.

Perhaps you might wish to think about the pros and cons of this system, for yourself.

In future, I will write more on how this new SEDE accounting system embodies principles of what some believe to be ‘sacred’ geometry, expressing the Grace (Mercy), Nurture, Wisdom and Beauty of the life-giving Female .. or Mother .. Nature.

******************

REFERENCES

[1] Galbraith, JK, Money: Whence It Came, Were It Went (1975), p. 15 – retrieved from Wikiquote August 2018

[2] McKay, Colin, deror.org, (2011)

[3] Becklumb, P., and Frigon, M., How the Bank of Canada Creates Money for the Federal Government: Operational and Legal Aspects (10 August 2015) – retrieved August 2018

[4] Nichols, D.M. and Gonczy, A.M.L, Modern Money Mechanics: A Workbook on Bank Reserves and Deposit Expansion (1994 edition), p. 6

[5] Investopedia: Promissory Notes – retrieved August 2018

[6] Financial Stability Board, Key Attributes of Effective Resolution Regimes for Financial Institutions (2014 revision) – retrieved August 2018

[7] Nichols, D.M. and Gonczy, A.M.L, Modern Money Mechanics: A Workbook on Bank Reserves and Deposit Expansion (1994 edition), p. 6

[8] Werner, R.A., A Lost Century in Economics: Three theories of banking and the Conclusive Evidence (2014)

[9] Angas, Major L.L.B. (Lawrence Lee Bazley), Slump ahead in bonds (1937), Somerset Pub. Co. pp. 20-21. (cited in Wikiquote, Banking) – retrieved August 2018

[10] Keynes, J.M., Newton, the Man, (c. 1946) – retrieved from University of St. Andrews History of Mathematics archive, August 2018

[11] King, L.W., The Code of Hammurabi, The Avalon Project, Yale Law School – retrieved August 2018

[12] Revue d’Assyriologie et d’archéologie orientale. Given intention to publish a book revealing further evidences, the author apologises for not providing a more detailed citation.

[13] ibid.

[14] Karpenko, V. and Norris, J.A., Vitriol in the History of Chemistry, Chem. Listy 96, 997-1005 (2002)

[15] ibid.

[16] Bossone, B. and Costa, M., Monies (Old and New) Through the Lens of Modern Accounting (2018), VOX CEPR – retrieved July 2018

[17] Fetter, F.A., Reformulation of the Concepts of Capital and Income in Economics and Accounting (1937) in “Capital, Interest, & Rent” (1977). via etymologyonline, Capital – retrieved August 2018

[18] Investopedia: Legal Tender – retrieved August 2018

[19] Oresme, N., Treatise on the Origin, Nature, Lw, and Alterations of Money (De origine, natura, jure et mutationibus monetarum), cited in Woodhouse, A. “Who Owns the Money?” Currency, Property, and Popular Sovereignty in Nicole Oresme’s De moneta (2017-18). Speculum. 92 (1): 85-116

[20] Bank of Canada, Backgrounders: Seigniorage, March 2013 (pdf) – retrieved August 2018

[21] Board of Governors of the Federal Reserve System, Federal Reserve Board issues interim final rule regarding dividend payments on Reserve Bank capital stock, Feb 18, 2016. – retrieved August 2018

[22] Board of Governors of the Federal Reserve System, FAQs – About the Fed: Who owns the Federal Reserve? – retrieved August 2018

[23] Bossone, B. and Costa, M., Monies (Old and New) Through the Lens of Modern Accounting (2018), VOX CEPR – retrieved July 2018

[24] Bakan, D., Sigmund Freud and the Jewish Mystical Tradition (1958). D. Van Nostrand Company Inc. New York. p. 204

[25] Oresme, N., cited in Rolnick, A.J., Velde, F.R., & Weber, W.E., The Debasement Puzzle: An Essay on Medieval Monetary History, Federal Rserve Bank of Minneapolis, Quarterly Review, Fall 1997 – retrieved August 2018 (pdf)

[26] Keynes, J.M., Economic Possibilities for our Grandchildren: Essays In Persuasion, The Future (1930) – retrieved September 2017

[27] Bernstein, J.L., The Checkered Career of Usury, American Bar Association Journal, Volume 51, September 1965. – retrieved August 2018

[28] Hudson, M., How Interest Rates Were Set: 2500 BC – 1000 AD (2000) – retrieved August 2018

[29] Karpenko, V. and Norris, J.A., Vitriol in the History of Chemistry, Chem. Listy 96, 997-1005 (2002)

[30] Scott, B., How to Burn Digital Money, 1 August 2018 – retrieved August 2018

[31] Assange, J., Conspiracy as Governance (2006) – retrieved Augsut 2018 (pdf)

[32] Shah, A.K., Big Four and the Revolving Door, Renegade Inc (2018) – watch online

[33] Whipple. J., The Importance of Usury Laws (1836)

Doublethink means the power of holding two contradictory beliefs in one’s mind simultaneously, and accepting both of them.

These contradictions are not accidental, nor do they result from ordinary hypocrisy: they are deliberate exercises in doublethink. For it is only by reconciling contradictions that power can be retained indefinitely. In no other way could the ancient cycle be broken. If human equality is to be forever averted—if the High, as we have called them, are to keep their places permanently—then the prevailing mental condition must be controlled insanity.

George Orwell, Nineteen Eighty-Four

Oh the irony.

Or perhaps rather, the karma.

From the birthplace of el modo vinegia (“the Venetian Method”) of Double Entry Bookkeeping, and the modern banking Usurocracy that it spawned more than half a millennium ago, comes academic confirmation of the “outright false accounting” and “double nature” of bank ‘money’.

Professor of Accounting Massimo Costa, along with former international financial markets professor and current World Bank and IMF advisor Biagio Bossone, have confirmed that so-called “money of account” created by Double Entry Bookkeeping is a “systematically concealed” tool for extracting “seigniorage rent” from the labour of the human race.

In academic jargon, it is “a structural element of subtraction of net real resources from the economy, with potentially deflationary effects on profits and/or wages, distributional consequences, and frictions between capital and labor.”

In other words, the global banking system is an enormous parasite, and its parasitic method is fraudulent.

Their article relates to the heart of my essays (eg, here, here, here, here, here) on the ancient, alchemical philosophistry – the word ‘magic’ with numbers added – on which the ‘modern’ banking system is built.

More generally, absent adverse economic or market contingencies inducing depositors to convert deposits into cash, the liabilities represented by deposits only partly constitute debt liabilities of the issuing bank, which as such require [central bank] reserve coverage. The remaining part of the liabilities is a source of income for the issuing bank – income that derives from the bank’s power to create money. In accounting terms, to the extent that this income is undistributed, it is equivalent to equity.

This double nature of demand deposits is stochastic in as much as, at issuance, every deposit unit can be either debt (if, with a certain probability, the issuing bank receives requests for cash conversion or interbank settlement) or equity (with complementary probability).

Despite the fact that they claim to have loaned us all this money, thanks to the magical paradox at the heart of double-entry accounting, they also claim, simultaneously, precisely the opposite to be true — that we have actually loaned all that money to them.

[..]

Believe it or not, there is an explanation—albeit a perverse, morally abhorrent and unconscionable explanation—for this, and in turn, for how the creeping global preparations to legally steal the “deposit” assets of bank customers (refer above diagram) is able to be “justified” by the banks, the financial and political authorities, and the unelected, BIS-funded, Goldman Sachs alumni-chaired FSB.

At the heart of the matter is the ever-present paradox of perspective inherent in the BabylonianDuality Principle on which double-entry accounting is based.

Banks are able to create new (so-called) ‘money’ ex nihilo through the loan origination process. As this is recorded using double-entry accounting, every new loan results in a new Asset and a new Liability on the banks’ balance sheet records.

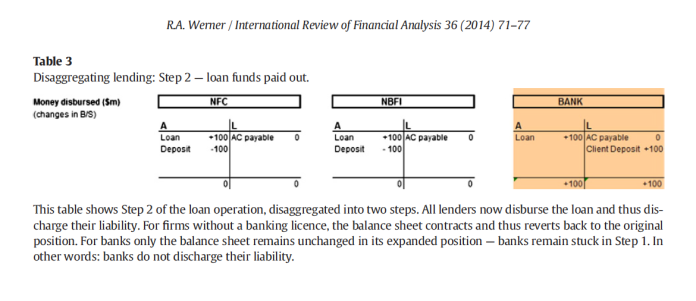

However, because banks act both as new loan (thus, new ‘money’) originators and as financial intermediaries, there is no way of disaggregating the Liability side of any bank’s balance sheet in order to clearly distinguish between those “deposits” that have arisen in consequence of that bank’s own lending (so-called), and those “deposits” that have arisen in consequence of that bank’s intermediation (i.e., ‘transfers’ of ‘money’ from one customer account to another customer account at the same bank, or, from the customer accounts of other financial institutions to customers of the bank).

Whether or not any particular unit of any particular “deposit” amount could truthfully be defined as ‘money’ loaned to the bank by a customer, or, loaned by the bank to a customer, is dependent on knowing with complete certainty how and when each and every unit came to be recorded in the customer account. The only customer account for which such certainty is possible, is a customer account created by the bank at the moment of first originating a loan, and, before any new entry for even one single fractional unit of the denominated currency has been either added to, or subtracted from that customer account.

There is one further exception – an account established for one of the bankers’ favourite clients—arms dealers, drug cartels, mafioso, and other criminal organisations such as the CIA—at the first moment of the client handing over real legal tender cash notes at the bank to open the account.

In any event, since even a ‘transfer’ of ‘money’ from one bank to another still has the same ultimate origin—an out-of-nothing creation of an electronic record of a mutual exchange of promises to pay—then from a whole-of-banking-system perspective it really doesn’t matter; all so-called ‘money’ on ‘deposit’ is simultaneously owned by the customers, and by the banks.

In other words, the global Usurocracy’s rent-extracting ‘money’ system is based on the arbitrary, subjective, relativist ‘logic’ and philosophistry of Cabala, or what George Orwell called doublethink – “the power of holding two contradictory beliefs in one’s mind simultaneously, and accepting both of them.”

Doublethink is related to, but differs from, hypocrisy and neutrality. Also related is cognitive dissonance, in which contradictory beliefs cause conflict in one’s mind. Doublethink is notable due to a lack of cognitive dissonance—thus the person is completely unaware of any conflict or contradiction.

Thanks to 503 years of “progressive” regulatory capture – amounting to nothing less than a thinly-concealed regime of state-sponsored Usurocracy – it is the banks’ exclusive privilege to ‘earn’ compounding usury on all the self-annihilating, +1|-1 Double Entry ‘money’ units that they create out of nothing:

Owing to double nature of commercial bank money, a relevant share of the deposits that banks report in the balance sheet as ‘debt toward clients’ generates revenues that are very much similar to the seigniorage rent extracted by the state through the issuance of state money (coins, banknotes, and central bank reserves).

Costa and Bossone confirm that it is precisely this “double nature” of bank ‘money’ that enables banks to hide the reality of their extracting “seigniorage rent” from the labour of the human race. How?

By not recording the value of their imaginary accounting ‘money’ – supposedly “equivalent” to, or, in more honest words, a counterfeit of, real physical government legal tender cash notes and coins – on their Income Statement:

Under current accounting practices, seigniorage is largely underappreciated, it is systematically concealed, and is not allocated to the income statement (where it naturally belongs), while it is recorded on the balance sheet under debt liabilities, thus originating outright false accounting.

As I extensively evidenced, this fraudulent system is actively aided and abetted by the “secretive”, tax haven-registered, “private” corporations of the international accounting standard-setters; a fact also confirmed – tacitly – by Costa and Bossone:

The stochastic double nature of bank money is consistent with the principles of general accounting as defined in the Conceptual Framework of Financial Reporting, which sets out the concepts underpinning the International Financial Reporting Standards (IFRS). In light of these standards, demand deposits are a hybrid instrument – partly debt and partly revenue. The debt part relates to the share of deposits that will (likely) be converted into cash or reserves, while the revenue part relates to the share of deposits that will (likely) never be converted into cash or reserves. This share of deposits is a source of revenue.

The Mercurial Rebis: A Crowned and Bat-winged Hermaphrodite, Buch der heiligen Dreifaltigkeit, late 14th Century (Munich MS, Bayerische Staatsbibliothek, CGM. 598). Source: Adam McLean, alchemywebsite.com

What Costa and Bossone (conveniently?) neglect to mention is that the share of so-called ‘deposits’ that “will (likely) never be converted into cash or reserves”, and that is thus “a source of revenue,” is around 97%.

Rather like the banks conveniently neglecting to mention the same 97% on their Income Statement.

Apparently it is sufficient to describe what is in reality the vast majority as merely “a relevant share”.

In “Dishonourable Debt” we saw that effective July 1, 2009 – in the middle of the global banking liquidity crisis known as the “GFC” – the Financial Accounting Standards Board (FASB) introduced Accounting Standards Codification (ASC) §305 Cash andCash Equivalents. This new standard effectively sanctioned – and further concealed – the banks’ misleading and deceptive conduct in renting their electronic records of promises to pay physical cash under the guise of so-called ‘money’. As I observed:

The FASB has ex post facto codified that banks may consider bank ‘credits’ (a record of a promise to pay cash) as actually being “cash” for accounting purposes; that the customers’ perspective of bank ‘credits’ “shall” be that those ‘credits’ are (literal physical) “cash”, and, that they are not amounts owed to them by the bank…

Pure Orwellian doublethink.

This should help us to understand the real reason why, for several decades, there has been an accelerating drive by the international banking system to ‘normalise’ numerous forms of electronic banking and ‘money’ – including crypto currencies – and more recently, to actively discourage and even to incrementally (“Boiling Frog” strategy) restrict or outright ban the use of physical cash.

Contrary to all propaganda, this carrots-and-sticks drive towards a global economy reliant on pure abstraction, rather than real physical currency, has nothing to do with improving “convenience” for the public, or “efficiency” in the banking system, much less with “fighting crime” or “the black market”.

Real physical cash – State legal tender – is perhaps the weakest link in the Usurocracy’s “golden chain” of Double Entry ‘magic’ enslaving the human race.

Real physical cash is what the Usurocracy is counterfeiting, using +1|-1 Double Entry nullities, and then “systematically” concealing by not reporting their counterfeit ‘cash’ on their Income Statements.

Once physical cash is eliminated, the promises-to-pay ‘money’ system will be fully “unfettered” and “independent” from the real, tangible world. It will exist solely in the abstract, “imaginary”, ‘magic’ paradox-riddled, counterfeit world (pun intended) of Double Entry Bookkeeping controlled by the Usurocracy.

“The bookkeeper can be king if the public can be kept ignorant of the methodology of the bookkeeping.”

Do read and share this outstanding resource compiled by Urunu: The Cashless Society.

This is in fact the formula of our Magick; we insist that all acts must be equal; that existence asserts the right to exist; that unless evil is a mere term expressing some relation of haphazard hostility between forces equally self-justified, the universe is as inexplicable and impossible as uncompensated action; that the orgies of Bacchus and Pan are no less sacramental than the Masses of Jesus; that the scars of syphilis are sacred and worthy of honour as much as the wounds of the martyrs of Mary.

..the existence of “Evil” is fatal to philosophy so long as it is supposed to be independent of conditions; and to accustom the mind to “make no difference”[1] between any two ideas as such is to emancipate it from the thralldom of terror.

The Magician should devise for himself a definite technique for destroying “evil”. The essence of such practice will consist in training the mind and body to confront things which cause fear, pain, disgust, shame and the like. He must learn to endure them, then to become indifferent to them, then to analyse them until they give pleasure and instruction, and finally to appreciate them for their own sake, as aspects of Truth.

Aleister Crowley, Liber V vel Reguli (Ritual of the Mark of the Beast) [2]

I will just say it.

The global accounting, banking, and ‘money’ systems, are Satanic.

All three systems are based on and operate according to fundamental principles that are identical to those in the philosophy and practice of satanism.

They are also identical to those in the “system of thought” that George Orwell described as doublethink.

An honest observer should be able to see this clearly, with a little thoughtful reflection.

According to a former priest in the (Anton LaVey) Church of Satan, the four main tenets of satanic ideology are:

Self-Preservation

Moral Relativism

Social Darwinism

Eugenics

These principles can be discerned in just one passage from the most notorious and influential Black Magician of the twentieth century:

We have nothing with the outcast and the unfit:

let them die in their misery. For they feel not. Compassion is the vice of kings: stamp down the

wretched and the weak: this is the law of the

strong: this is our law and the joy of the world.

Think not, o king, upon that lie: That Thou

Must Die: verily thou shalt not die, but live.[3]

This is emphasised by the Fraternitas Saturni (Brotherhood of Saturn) in an oxymoronic, ‘blackwhite’ expansion on Crowley’s dictum “Do as thou wilt shall be the whole of the Law”:

Love is the Law, Compassionless Love.[4]

‘Art’ work allegedly owned by John Podesta. Note colours: ‘white’ demon (with Male, red-haired child) on Left; ‘black’ demon (with Female, white-haired child) on Right.

In Thus Spoke Zarathustra: A Book for All and None, nihilist philosopher Friedrich Nietzsche equated pity with self-annihilation.[5] For the satanist, or Black Magician, rejection of pity is “the magical equivalent of the rejection of self-annihilation.”[6]

In other words, to “emancipate” or “liberate” oneself entirely from the “bond” of compassion, of empathy for other beings, is seen as an act of Self-Preservation.

In our time compassion is even forbidden by science, as is already happening in England, where they have political economy.

‘Modern’ accounting, banking, and ‘money’ – the foundations of global finance, markets, economic and political life – all operate on the Double Entry Bookkeeping system.

Many historians and economists, including (eg) Werner Sombart, Max Weber, and Joseph Schumpeter, have traced the development of modern capitalist business practice to the Double Entry system, attributing to it the “pitiless” spirit of modern commerce in its “unending, systematic pursuit of profit”:

In [Schumpeter’s] view, double entry’s “cost-profit calculus” drives capitalist enterprise – and then spreads throughout the whole culture: “And thus defined and quantified for the economic sector, this type of logic or attitude or method then starts upon its conqueror’s career subjugating – rationalizing – man’s tools and philosophies, his medical practice, his picture of the cosmos, his outlook on life, everything in fact including his concepts of beauty and justice and his spiritual ambitions.” For Schumpeter, capitalism “generates a formal spirit of critique where the good, the true and the beautiful no longer are honoured; only the useful remains – and that is determined solely by the critical spirit of the accountant’s cost-benefit calculation”.[7]

Karl Marx – the 19th century arch materialist – stated that accounting is even “more necessary” for a communist system:

As unity within its circuits, as value in motion, whether in the sphere of production or in either phase of the sphere of circulation, capital exists ideally only in the form of money of account, primarily in the mind of the producer of commodities, the capitalist producer of commodities.

Bookkeeping, as the control and ideal synthesis of the process, becomes the more necessary the more the process assumes a social scale and loses its purely individual character. It is therefore more necessary in capitalist production than in the scattered production of handicraft and peasant economy, more necessary in collective production than in capitalist production.[8]

As we have seen in previous essays (here, here), Double Entry Bookkeeping was not created as a neutral, objective tool for value-adding producers or manufacturers to manage their costs. It was developed by merchants (traders) from the dawn of mercantile capitalism, as a tool whose real “use” value was to conceal their illegal practice of usury from Church-State authorities. It also served as a psychological tool of self-deception, enabling the merchant to convince himself that his actions were morally (thus ‘divinely’) justified – as “proved” by his meticulously-recorded and balanced books.

Merchants or traders have been condemned by true sages and religious divines throughout history and across many cultures, because their actions were seen as parasitic, and immoral; not adding to the common wealth of society, but merely taking from that produced by others.[9] The merchant is an intermediary, a middleman between producer and consumer, who aims to “buy low and sell high”, whether by fair means or foul (hello storytelling: advertising, marketing, “Public Relations”). He profits in whole or in part through taking advantage of what many today euphemistically call “information asymmetry” – which in other, more honest words, means the relative (to oneself) ignorance of others.

Double Entry embodies the satanic doctrine of Self-Preservation. The goal of the Black Magician is to become ‘as god’ – the Absolute, the One, the All, the Nothing, the ‘Divine Mind’ or ‘Pure’ Intellect – without sacrificing* his or her “individuated existence”.

(*The exact opposite of the Christian doctrine of self-sacrifice, and its ultimate aspiration of self-less union with, or complete self-annihilation in, the Divine; e.g., Matthew 16:20-25.)

Double Entry is a numeric and sophistic tool of control over the real or imagined events of the past, present, and future. It offers the possibility of becoming ‘as god’; of attaining Ultimate Power over the material realm (“Money Power”), which the magician equates with power over the imaginary (‘divine’ mind) realm as well.

This serpent, SATAN, is not the enemy of MAN, but HE who made Gods of our race, knowing Good and Evil; He bade ‘Know Thyself!’ and taught initiation. He is ‘the Devil’ of the Book of Thoth and His emblem is BAPHOMET, the androgyne who is the hieroglyph of arcane perfection.[10]

According to Lewis Mumford (Myth of the Machine), accounting’s “concentration on abstract pecuniary rewards” – Profit (or Loss) – “introduced a driving motive into daily life, equivalent on its own base level to the monk’s search for an eternal reward in Heaven. The pursuit of money became a passion and an obsession: the end to which all other ends were means.”

Double Entry Bookkeeping also embodies the satanic doctrine of Moral Relativism.

The core of Crowley’s magical philosophy is the willed dissolution of opposites – “Let there be no difference … between any one thing and any other thing.” – in greater unity (agape, love).[11]

[As we have seen, ‘love’ in satanic doctrine is “Compassionless”, “pitiless”.]

Every single transaction recorded by Double Entry, is entered twice. The one action or event (real or imaginary) is dissolved or divided into two records which, in effect, cancel out or an-nihil-ate each other: a debit entry, and an equal and opposite credit entry.

Debits must equal Credits.

Negatives must equal Positives.

‘Evil’ must equal ‘Good’.

Black must equal White.

The union of both – the “sacred marriage” or “union of opposites” – equals Nothing:

I am God, I very God of very God; I go upon my way to work my Will; I have made Matter and Motion for my mirror; I have decreed for my delight that Nothingness should figure itself as twain… [two]

I am the None, for all that I am is the imperfect image of the perfect; each partial phantom must perish in the clasp of its counterpart, each form fulfil itself by finding its equated opposite, and satisfying its need to be the Absolute by the attainment of annihilation.

The World LAShTAL includes all this.

LA—Naught.

AL—Two.

LA … represents the Ecstasy of Nuit and Hadit conjoined, lost in love, and making themselves Naught thereby. [..]

AL, on the contrary, though it is essentially identical with LA, shows “The Fool” manifested through the Equilibrium of Contraries. The weight is still nothing, but it is expressed as it were two equal weights in opposite scales. The indicator still points to zero.

[“ShT” is “Fire” (Sh) and “Force” (T); it “expresses the secret nature which operates the Magick or the transmutations.” Abbreviation of “Shaitan”; Satan.][12]

The Fool, Thoth Tarot deck, Aleister Crowley’s Book of Thoth, Liber LXXVIII. (Source: bibliotecapleyades.net)

The Double Entry system embodies what George Orwell referred to in his dystopian novel Nineteen Eighty-Four as “the system of thought which really embraces all the rest, and which is known in Newspeak as doublethink [..] a vast system of mental cheating”:

Doublethink means the power of holding two contradictory beliefs in one’s mind simultaneously, and accepting both of them.[13]

The key word here is blackwhite. Like so many Newspeak words, this word has two mutually contradictory meanings. Applied to an opponent, it means the habit of impudently claiming that black is white, in contradiction of the plain facts. Applied to a Party member, it means a loyal willingness to say that black is white when Party discipline demands this. But it means also the ability to believe that black is white, and more, to know that black is white, and to forget that one has ever believed the contrary.[14]

The Double Entry system also embodies another “essential” principle of Satanism, and applies it in the same way, for the same purpose: as its means to an end – the practice of Antinomianism.

The [left-hand path] practice .. often manifests itself in antinomianism, that is, the purposeful reversal of conventional normatives: ‘evil’ becomes ‘good,’ ‘impure’ becomes ‘pure,’ ‘darkness’ becomes ‘light’.

In [Crowley’s] “theology” the results of the application of this antinomianism are that opposites, such as the Beast and the Lamb (Rev. 13:8) and the Whore of Babylon and the Woman clothed with the Sun (Rev. 12:1) are only apparent, and that from a higher perspective they are unities or equivalencies (Beast = Lamb; Whore = Woman).

LaVey sees as natural [the] indulgence in all the so-called seven deadly sins of Christianity: greed, pride, envy, anger, gluttony, lust and sloth. Each of which he views as a possible catalyst for positive and natural human activities or attitudes … (See the Satanic Bible, ch. III). The fact that most people today, and the whole “western industrialized economy” is really driven by the desires of the masses to indulge in all of the seven deadly sins is a powerful argument for the presence of a Satanic Age.[15]

The capitalist scheme of values in fact transformed five of the seven deadly sins of Christianity – pride, envy, greed, avarice, and lust – into positive social virtues, treating them as necessary incentives to all economic enterprise; while the cardinal virtues, beginning with love and humility, were rejected as ‘bad for business,’ except in the degree that they made the working class more docile and more amenable to cold-blooded exploitation.[16]

Double Entry causes much confusion (“Babel”, from Hebrew בָּלַלbalal, Babylon), not only with beginners (‘novice’, ‘apprentice’) but even with experienced practitioners (‘adept’). The reason why is because its ‘logic’ is the exact opposite of what a normal person would naturally expect, based on the words used.

In common understanding, the word “credit” implies something Good. A positive. Something that adds to, increases, or improves. “Well done! That work is a credit to you.”

A “debit”, on the other hand (see etymology), is commonly understood to mean the exact opposite; something Bad. A negative. A loss, deficiency, or deficit. “On the biographical debit side there are the usual miscellaneous acts of thoughtlessness, rudeness and generally shabby behaviour.”

In Double Entry, however, the operating ‘logic’ is reversed. In its fundamental process – recording entries – words actually mean the exact opposite of what we normally understand them to mean.

A “debit” does not subtract (-) from an account. It adds to it (+).

A “credit” does not add (+) to an account. It subtracts from it (-).

(That is, for an Asset account. For a Liability account, the same words mean the reverse: a “debit” subtracts, and a “credit” adds. Doublethink.)

The satanic principle and practice of antinomianism – the deliberate inversion or reversal of values and conventions; the breaking of rules, laws, taboos – is embedded in Double Entry’s basic operation.

It is pitiful to see, how strangely some Men of Quality and Fortune, are to seek in Accompts; and how they are blinded and bambouzled by the Mists, that artful Men raise up before their Eyes, with Estimates, as they call ’em, and Representations of Values, drawn out of immense Books of Accompts, while the proper Judges know the Way neither into, nor out of them, and listen to the Jargon, as if it were Coptick, or Arabick.

Roger North, The Gentleman Accomptant, 1714

“For every debit there must be a credit, and for every credit there must be a debit” – Alas! How few consider that if this must be the case, the rule to go by, nothing is more easy than to make a set of books wear the appearance of correctness, which at the same time is full of errors, or of false entries, made on purpose to deceive!

Edward Thomas Jones, Jones’ English System of Book-Keeping by Single or Double Entry, 1796

The whole difference, and the only difference, between the two systems of accounting is in the fact that single-entry bookkeeping always uses literal language, while double-entry bookkeeping always uses figurative language except when speaking of persons.

In single-entry bookkeeping, cash means cash. Merchandise means merchandise. Interest means interest. Expense means expense. But in double-entry bookkeeping cash does not mean cash; it means the imaginary person who owes the amount of the cash. Merchandise does not mean merchandise; it means the imaginary person who owes the amount of the merchandise. Interest does not mean interest; it means the imaginary person who owes or is owed the amount of the interest. Expense does not mean expense; it means the imaginary person who owes the amount of the expenses. Net Capital does not mean net capital; it means the person (real in the case of an individual owner, imaginary in the case of a firm or a corporation) who is owed or owes the amount of the net capital.

Charles M. Van Cleve, Principles of Double Entry Bookkeeping, 1913

A good tree cannot bring forth evil fruit, neither can a corrupt tree bring forth good fruit.

Every tree that bringeth not forth good fruit is hewn down, and cast into the fire.

Consider closely “The Fool” (‘0’) tarot card (shown above), as designed by Aleister Crowley. His exposition of its symbolism can be found here.

At some point in future, I hope to discover the necessary motivation to begin the task of elaborating on the colour green and its far-reaching symbolic significance, not only as the “colour of money”, but also in alchemy, Cabala, sex ‘magick’, human biology, chemistry, metallurgy, and in Hollywood movie ‘entertainment’.

UPDATE 8 June 2018: included clarification (in parentheses) regarding the opposite application of debits and credits for Asset and Liability accounts.

**********************

REFERENCES